Subscribe (free) to xpostfactoid

As xpostfactoid is devoted mainly to tracking the implementation and metamorphosis of the Affordable Care Act, for the past two years I've focused mainly on ACA programs' performance as a safety net during the pandemic, as millions of people lost job-based health coverage for varying lengths of time.

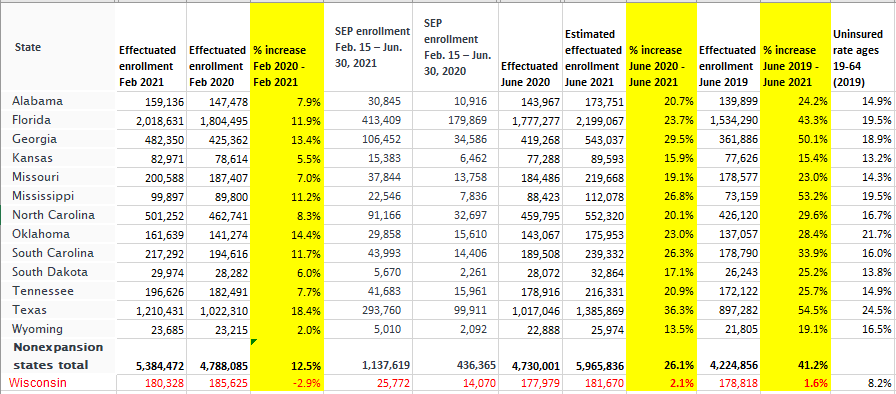

In 2020, the uninsured rate appears to have remained basically flat, though pandemic-related surveying challenges rendered Census and NHIS findings somewhat tentative. In 2021, the uninsured rate may actually prove to have downticked a bit, once the data is in. By kludgy American standards, the health insurance safety net -- Medicaid and the ACA marketplace -- have performed well, bolstered by several doses of emergency legislation and administrative action:

- The Families First Act, which added six percentage points to the federal government's share of Medicaid costs -- contingent on states pausing Medicaid "redeterminations" and disenrollments for the duration of the COVID-19 emergency (still in effect).

- Belated ACA Medicaid expansions that went live in Idaho, Utah and Nebraska in 2020 and in Oklahoma and Missouri in 2021.