Subscribe (free) to xpostfactoid

Health insurance broker Jenny Chumbley Hogue, based near Dallas, highlights one good thing about the longer Open Enrollment Period for the ACA marketplace enacted by the Biden administration (OE is now running through January 15 rather than December 15):

That is: Marketplace enrollees who passively let themselves be auto-re-enrolled for 2022 in their current plan, and get shocked in January by a sliding benchmark that raises their premiums (sometimes dramatically), can now choose a cheaper plan before January 15 and suffer only one month at the higher premium, rather than being locked in for twelve months.Thank goodness OEP extended to 1/15 so we can correct the issues. @charles_gaba @LouiseNorris @AlekaGurel @xpostfactoid @SheronESidbury

— Jenny Chumbley Hogue (@kgmom219) December 13, 2021

At an income of $25,000 for a couple -- just under 150% FPL -- the benchmark (second cheapest) silver plan is free in 2021 and 2022, thanks to the subsidy boosts created by the American Rescue Plan Act, enacted in March 2021 (the ARPA Jenny Hogue refers to in the tweet). That is, at least two silver plans are free for any individual or family with an income up to 150% FPL.

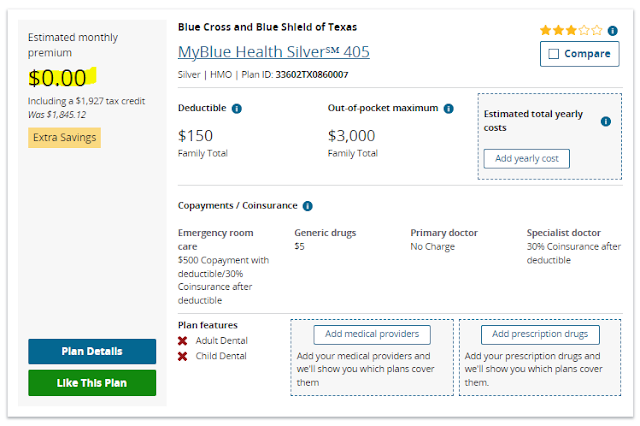

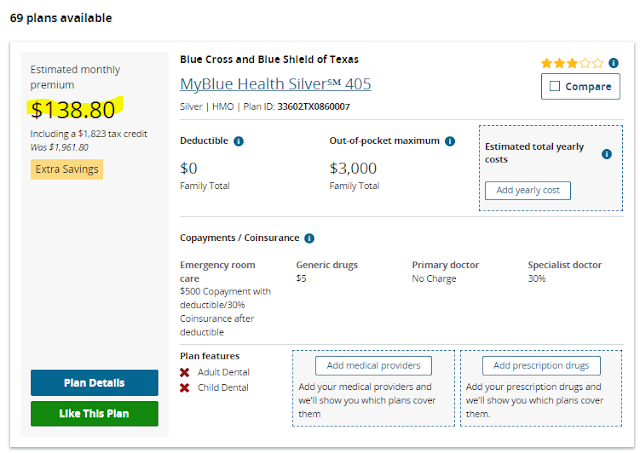

This year, the cheapest silver plan in Dallas was the Blue Cross plan shown below. But see what happens to a pair of 63 year-olds in Dallas who renew that plan in 2022:

2021

2022

Add a 23 year-old dependent, and the premium goes to $160/month in 2022 -- close to Jenny Hogue's generic example.

How does this happen? To back up, briefly: ACA premium subsidies are designed so that the enrollee pays a fixed percentage of income (ranging from 0 to 8.5% in 2022) for the benchmark second-cheapest silver plan. If the benchmark in 2022 has a lower (unsubsidized) premium than the benchmark in 2021, the subsidy goes down. If your 2021 plan's premium goes up, it's a double whammy.

The whiplash is more intense for older enrollees. Since premiums rise with age, and the subsidy rises to cover the difference for the benchmark plan -- a 64 year-old pays the same for the benchmark as a 21 year-old, though the unsubsidized premium is three times as high. But if the 64 year-old buys a plan that costs more than the benchmark, she'll face a wider spread -- and so, a larger increase --than the 21 year-old.

Last year, the Blue Cross plans shown above was the lowest-cost silver plan in Dallas -- and so doubtless attracted a lot of enrollment. This year, three cut-rate insurers -- Bright HealthCare, Friday Health Plans, and Ambetter -- put up ten silver plans cheaper than Blue Cross's cheapest (the same plan that was this year's lowest-cost silver plan). Meanwhile, Blue Cross raised the premium for this plan by 6%.

For two 63 year-olds with an income of $25,000, the unsubsidized premium for the benchmark silver plan in Dallas dropped by $105/month year-over year. In 2021, the Blue Cross plan was well below the benchmark; in 2022, for two 63 year-olds, it's a $139/month above it, and they pay the difference. Two 40 year-olds would face a narrower spread, and pay $59/month for the Blue Cross plan in 2022.

In 2021, 29% of all marketplace enrollees -- almost 4 million -- were auto-enrolled. That is, they let their 2020 plans renew passively. Most weren't slammed to the extent illustrated above. But auto-enrollment is always dangerous.

The selection in Dallas, as in many markets, is complicated by excessive choice. There are 69 silver plans available, compared to 36 last year (sorry, I neglected to capture that in the 2021 screenshot). Bright HealthCare alone offers six silver plans cheaper than the cheapest Blue -- all with the same HMO provider network. That's obscene: it makes a mockery of the ACA requirement that separate plans offered in the same area by one insurer be "meaningfully different" from one another.

For most enrollees, choice is limited by price -- if they venture to look at offerings. Most low-income people are not going to accept a $139/month premium increase if there's a more or less comparable alternative close to what they were paying previously. But the chaos of a market with 164 plan choices -- on offer in Dallas for 2022 -- may scare some people off. And auto-enrollment -- this year and every year -- is dangerous.

Good to have a broker like Jenny Hogue to hound you to check your options -- and to help you sort through them. For that matter, HealthCare.gov (and the state exchanges) will hound you too:

See Louise Norris for other reasons to actively enroll or re-enroll before Dec. 15 (tomorrow!)

Great summary as always. I could not avoid noticing that this couple is getting an annual federal subsidy of about $24,000 in any scenario. Of course in two years when they turn 65, they will get a similar subsidy thanks to full Medicare.

ReplyDeleteWe are assuming in all this that the couple has enough assets to actually live on a joint income of $25,000 a year.