11/19: See update at bottom: Healthcare.gov put out an email today that leads with nonprofit assisters

Obtaining health insurance from publicly supported programs in the U.S. is a complex process, necessarily supported by a variegated ecosystem of enrollment assisters. For people under age 65, nearly 50,000 commercial health insurance brokers and agents are registered (as of 2020), along with about 30,000 nonprofit enrollment assisters (as of 2016), many of the latter supported by federal or state funding.

Enrollment of the under-65 population that lacks access to employer-sponsored insurance depends on both commercial and nonprofit assisters, who have different and to some extent complementary strengths and weaknesses.

Nonprofit navigators and Certified Application Counselors (CACs) are certified and trained by the federal government, or by state governments in 18 states (including D.C.) that now run their own ACA exchanges. They are mandated by statute and trained to accommodate vulnerable and underserved populations, to provide culturally sensitive assistance, particularly to people with limited English proficiency, and to present all options without making a positive recommendation. They receive no compensation from insurers and depend either on government funding (navigators and assisters in Federally Qualified Health Centers) or nonprofit funding sources (CACs).

Agents and brokers do make positive recommendations; they are funded by insurer commissions and sometimes work for only one or in any case not all insurers selling on-exchange plans in a given area. They cost government nothing but may not offer unbiased information. They can be unscrupulous, pushing people into ACA-noncompliant plans that offer skimpy and unreliable coverage, and, alternatively, they can be worth their weight in gold. They are required by some but not all states to act in the client's best interest.

The Trump administration declared war on nonprofit assisters, reducing funding for the federal navigator program (operating in states that use the federal exchange, HealthCare.gov) by 84%, from $63 million in 2016 to $10 million in 2018 and years following (state-based exchanges have their own funding base for enrollment assistance, gleaned from user fees charged to insurers participating on the exchange). Under the leadership of Seema Verma, CMS maligned and slandered the navigator program, exploiting weaknesses in the program's data reporting and ignoring the fact that in many states navigators, who primarily serve low income people, enroll more people in Medicaid than in marketplace plans.

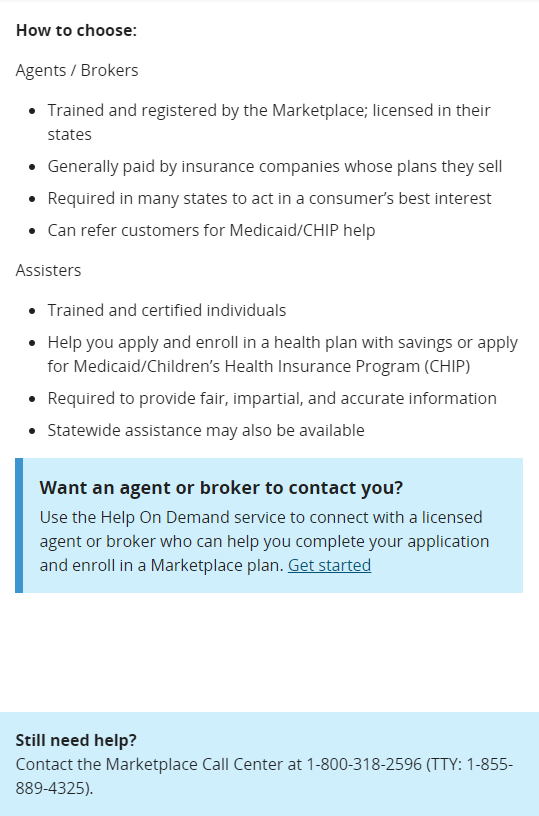

On the other side of the ledger, the Trump administration bulked up broker capabilities in ways the Biden administration is unlikely to jettison. They encouraged continuing development of a Direct Enrollment program, through which commercial online brokers and insurers could take online applications and process subsidies. This system is dominated by HealthSherpa, an excellent online enrollment platform that thousands of brokers can use and brand privately, and which most insurers that have registered as Direct Enrollment providers also license. In 2021, HealthSherpa processed about 23% of all enrollments on HealthCare.gov. The Trump administration also developed a Help on Demand program, administered by a private contractor, through which a visitor to HealthCare.gov can request assistance and be contacted by an agent or broker within 30 minutes. In 2020, Trump's CMS boasted, brokers assisted just shy of half of all enrollments on HealthCare.gov. (Conversely, a 2016 KFF study estimated that nonprofit assisters helped about 5.3 million people in Open Enrollment for 2016.)

The Biden administration reversed the depredations suffered by the navigator program, allocating more than $90 million dollars to 60 navigator groups for the Open Enrollment season that began on November 1, along with an enhanced advertising/marketing budget.

But the Biden administration has not reversed the inherited tilt of HealthCare.gov toward assistance from commercial brokers and agents. As someone with a dormant login to HealthCare.gov, I have received the email pitch below six times since Open Enrollment for 2022 began (my emphasis):

That is a deployment of the Help on Demand program mentioned above, which deploys commercial brokers and agents only. Clicking through takes you to a Help on Demand form. Hence the exclusive mention in the main body of the pitch of agents or brokers, excluding navigators and CACs.

At the very bottom, the pitch does provide this backhand allusion to the nonprofit assistance universe:

I believe there is a lot of state-by-state variation on this issue. In 2016-2017, when I was an agent, many insurers stopped paying any commission on ACA policies. In other states, $9 per month was not uncommon.

ReplyDeleteAgents for individual health insurance disappeared in those places. (other than for sleazy short term insurance, which continues to pay about 15% of premium to agents.)

The big outfits like Health Sherpa might have enough economies of scale to survive on small commissions.

I just don't know. Not your fault, because this data is hard to find.