My last post involved a close look at the severely tiered provider network in the silver plans sold in the ACA marketplace by Independence Blue Cross, the dominant insurer in Philadelphia and southeastern Pennsylvania. On a second look, a thought occurred to me: tiered networks that place go-to hospitals in higher tiers put an asterisk of sorts on balance-billing protections for emergency care, including those due to come online nationally when the No Surprises Act takes effect on January 1.

Under the No Surprises Act, emergency care is billed at in-network rates whether or not the hospital or facility is within the provider network of the patient's health plan. But what exactly is an "in-network rate" in a tiered network? Depends on the tier.

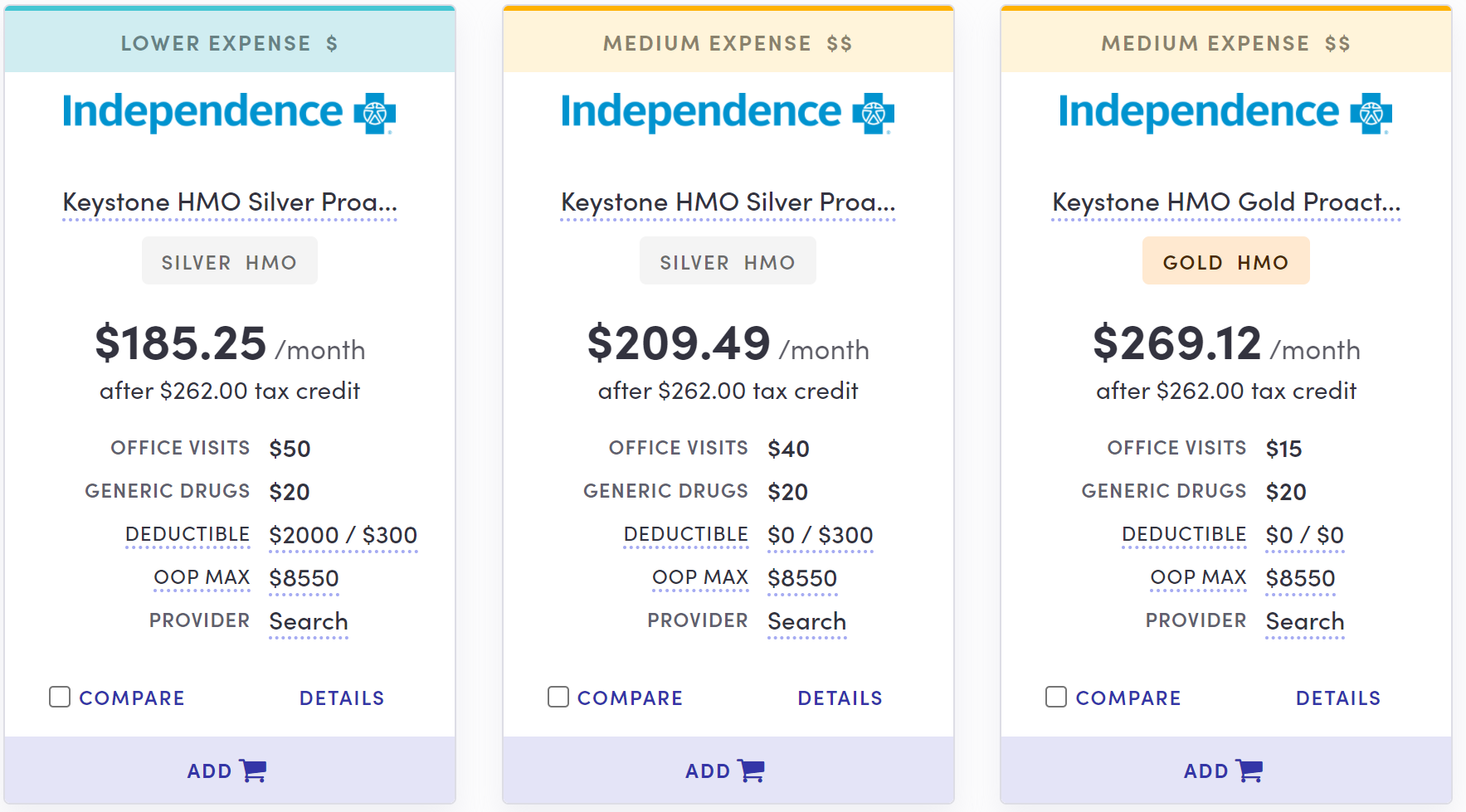

Independence's HMO plans sold in the ACA marketplace have three tiers. Its second-cheapest silver offering on Pennie, Pennsylvania's ACA exchange, the Keystone HMO Silver Proactive plan, posts a deductible of $0. But that's in Tier 1 only. For enrollees with incomes too high to qualify for Cost Sharing Reduction (CSR),* Tiers 2 and 3 have a deductible of $6,000 for an individual and $12,000 for a family.