As I noted in my last post, the American Rescue Plan Act's boosts to ACA marketplace subsidies seem to have reversed a years-long slide in "CSR takeup" among low-income enrollees. That is, during the emergency Special Enrollment Period that ended this past August 15, about 90% of enrollees with incomes below 200% of the Federal Poverty Level selected silver plans and accessed strong Cost Sharing Reduction (CSR), up from about 77% in the last Open Enrollment period. CSR is available with silver plans only. At incomes up to 200% FPL, it raises the value of a silver plan to the rough equivalent of platinum at no extra cost to the enrollee.

The surge in silver selection at low incomes this spring and summer was only logical, since ARPA made a benchmark silver plan free at incomes up to 150% FPL, and available for no more than 2% of income at incomes up to 200% FPL ($25,520 for a single person in 2021). At incomes below 200% FPL, CSR reduces deductibles and out-of-pocket maximums to a small fraction of those prevalent in bronze plans (the median deductible obtained by 2.1 million enrollees on HealthCare.gov during the SEP was $50; bronze deductibles average nearly $7,000). Free bronze plans used to be a serious temptation at incomes between 150-200% FPL in particular; now, not so much.

Since bronze plans are now almost always "dominated" by silver plans at incomes up to 150% FPL, and almost always a poor choice up to 200% FPL, I thought I'd check the degree to which the ACA exchanges - -HealthCare.gov, now serving 33 states, and 18 state-based exchanges (including D.C.'s) steer low-income enrollees toward silver plans.

The news on that front is fairly good. The newer state-based exchanges, and some that have upgraded their software, default to showing available plans in descending order by lowest expected overall costs -- premium plus out-of-pocket, based in part on the user's reported expectations as to how much medical care they'll need (e.g., estimates of doctor visits and prescriptions per year). At incomes up to 150% FPL, this puts lowest-cost silver plans above lowest-cost bronze by default: both will be $0 premium, but silver out-of-pocket costs will be lower.

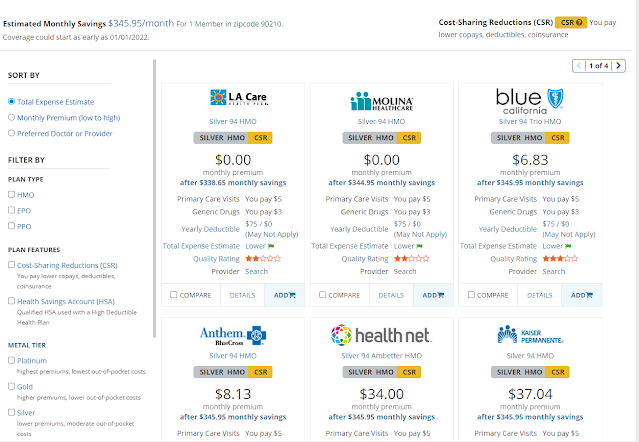

Here are the first plans viewable on Covered California's "shop and compare" tool for a 40 year-old with an income of $19,000 (just under 150% FPL) in zip code 95834 (Sacramento County). Pennie and GetCoveredNJ, state-based exchanges for Pennsylvania and New Jersey launched in 2020, take a similar approach.

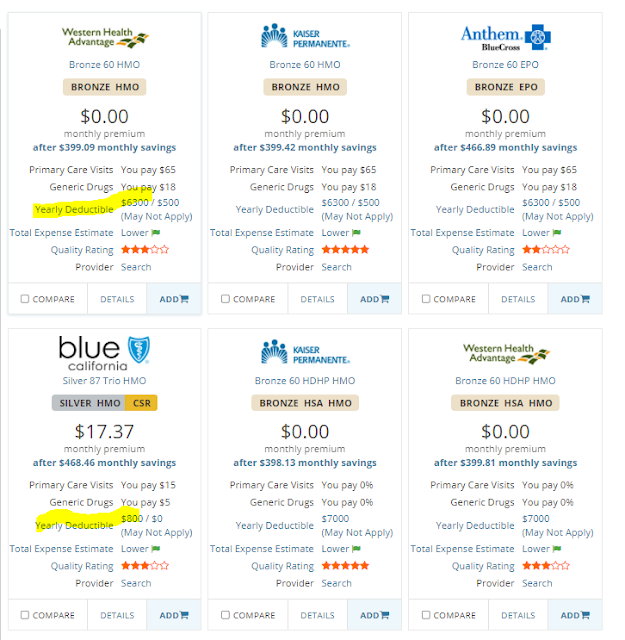

In my opinion these cost estimating tools have a weakness, though: they don't factor in risk. At an income of $25,000, just below 200% FPL, where CSR is still strong, if you indicate that you anticipate light use of medical services, the tool will put bronze plans first:

Note the deductible difference: $800 vs. $6,300 (or $7,000 for bronze HSA plans). The out-of-pocket maximum at this income level is $2,850 for CSR-enhanced silver, $8,200 for bronze (or $7,000 for HSA bronze). Saving $200 on the premium puts you at risk of more than $5,000 extra expense if you have a serious medical need. A significant percentage of enrollees in the 150-200% FPL range, where premiums for a benchmark silver plan top out at $43/month for individual, still select bronze plans. That's not good.

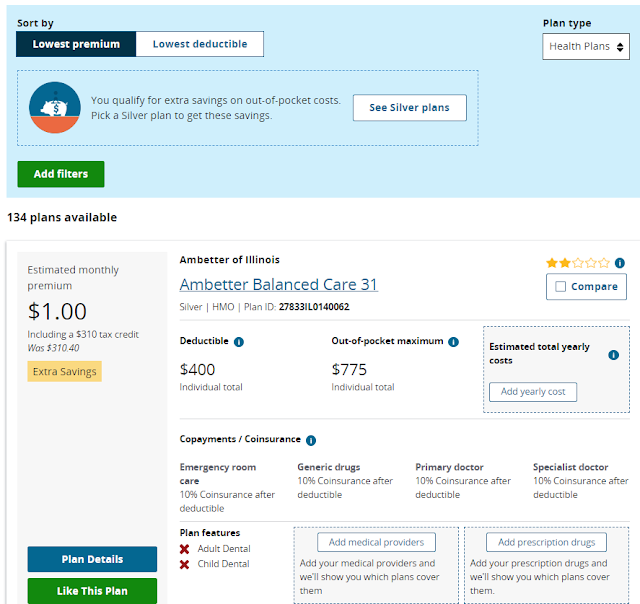

HealthCare.gov, serving 33 states this year, takes a somewhat different approach. By default, it lists plans by premium, lowest to highest. But it heavily signposts the value of CSR. And at incomes up to 150% FPL, it places zero-premium silver ahead of zero-premium bronze. Here is what comes first in the "shop and compare" tool (after a separate notice about CSR) for a single 40 year-old with an income of $19,000 in Cook County, IL (the $1.00/month is a mandatory separate fee for abortion coverage):

In the 150-200% FPL range, the message is more mixed. There's the invitation to filter for silver, but bronze plans appear on top:

No comments:

Post a Comment