Note: All xpostfactoid subscriptions are now through Substack alone (still free), though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up!

Today is the ACA’s 13th birthday, and CMS released its final enrollment report and detailed enrollment data for the 2023 Open Enrollment Period (OEP) in a celebratory vein. The good news: Enrollment nationally overall is up 13% year-over year and 36% since 2021, after two years with premiums subsidies substantially boosted by the American Rescue Plan Act of March 2021. (As I noted here when OEP was mostly completed, enrollment growth is heavily concentrated in the twelve states that had not enacted the ACA Medicaid expansion as of OEP 2023.) New enrollment increased by 21%.

In OEP 2022 — the first OEP in which there was no income cap on subsidy eligibility — enrollment growth was highest at high incomes. In marked contrast, this year it’s concentrated at low incomes. In the 33 states that use HealthCare.gov (which include all of the twelve states that haven’t expanded Medicaid), enrollment at incomes between 100% and 150% of the Federal Poverty Level (FPL) increased from 32% of all enrollment in 2022 to 37% this year, rising 20.4%, from 4,640,092 in OEP 2022 to 5,588,315 million in 2023.

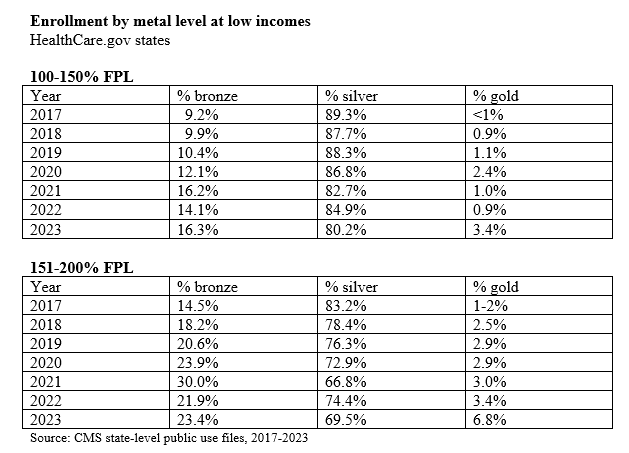

While increased enrollment at low incomes is good news, there is a disturbing aspect to the surge: Far too many enrollees with income below 200% FPL declined to select silver plans, and so did not avail themselves of the strong Cost Sharing Reduction (CSR) that attaches to silver plans — and only silver plans — at incomes below that threshold.

The ARPA subsidy boosts, implemented in March 2021, dropped the premium for a benchmark silver plan (the second cheapest silver plan in each rating area) to $0 for enrollees with incomes up to 150% FPL ($20,385 for an individual, $41,625 for a family of four in OEP 2023), rising to 2% of income (about $45/month for a single enrollee) at 200% FPL ($27,180 for an individual, $55,500 for a family of four). After several years of decline, silver plan selection rose slightly in 2022, the first OEP with the reduced premiums — but dropped to its lowest point ever at incomes up to 150% FPL this year, and to the second lowest level ever in the 150-200% FPL range.

CSR raises the actuarial value of a silver plan from a baseline of 70% (silver with no CSR) to 94% for people with income up to 150% FPL, and to 87% for enrollees in the 150-200% FPL income range. That’s as compared to 60% AV for a bronze plan and 80% for gold. The average silver plan deductible in 2023 is $108 at incomes up to 150% FPL and $567 at incomes in the 150-200% FPL range — compared to $7,481 for bronze and $1,650 for gold.

Differences between CSR-enhanced silver (at incomes below 200% FPL) and other metal levels in annual maximum out-of-pocket costs (MOOP) are equally stark. The MOOP averages $1,321 in silver plans at incomes up to 150% FPL and $2,747 for silver in the $150-200% FPL range. Bronze plan MOOP usually tops $8,000 (except in HSA-compatible plans, where it’s capped at $7,500), and in most gold plans as well. Low-income enrollees who forgo CSR are exposing themselves to thousands of dollars in potential out-of-pocket costs from which CSR in silver plans would protect them (if they stay in-network when obtaining care).

From 2018 through OEP 2021, bronze plan selection at low incomes increased every year in part because silver loading, the marketplace response to Trump's cutoff of direct reimbursement of insurers for CSR, made bronze plans free to a majority of buyers with income below 200% FPL. In some states and counties, silver loading has also made gold plans cheaper than silver plans, since CSR boosts the average actuarial value of a silver plan to a level above the gold AV (80%).

Some states — notably joined by Texas in 2023 — now require insurers to price gold plans below silver plans, and very cheap gold plans in Texas (where enrollment spiked 31% in 2023) boosted gold plan selection at incomes below 200% FPL and particularly in the 150-200% FPL range to far above normal levels for those income groups. Fully a quarter (24.6%) of Texas enrollees in the 150-200% FPL range selected gold plans, as did 19.4% 13.9% of Texas enrollees with income below 200% FPL (including those below 150% FPL). In fact, in the 33 HealthCare.gov states, Texas accounts for 71% of gold plan selection at incomes below 200% FPL (245,000 out of 344,000 gold enrollees below the 200% FPL threshold).

Premiums for some silver plans can be substantial for enrollees in the 150-200% FPL, and in some cases, cheap gold may be a reasonable choice — particularly if an insurer with a must-have network prices silver well above benchmark. In some few cases, even at incomes below 150% FPL, the need to obtain a provider network suited to the enrollee’s needs may even motivate a bronze choice. That said, the fact that 20% of enrollees with income below 150% FPL passed up high-CSR silver — including at least two free silver plans — indicates that something is going wrong with marketplace presentation of plan options

One factor may be the almost cancerous proliferation of plan choices in the last few years (discussed here), coupled with flawed choice architecture (discussed here) in the exchanges (though we are dealing here only with HealthCare.gov states, and HealthCare.gov’s signposting of CSR has not changed significantly). Also, metal level selection patterns may be different in the 18 state-based marketplaces, for which less detailed data is available.

Perhaps the increase in new enrollees has something to do with the low silver selection. In HealthCare.gov states, 75% of new enrollees with income below 150% FPL chose silver, compared to 85% of active re-enrollees (those who logged on, updated their information and made a positive choice) and 71% of passive, auto-re-enrollees. At 150-200% FPL, 62% of new enrollees chose silver, vs. 74% of active re-enrollees and 63% of passive re-enrollees. I recall from Covered California’s enrollment data that new enrollees in that state tend to select silver at lower levels than re-enrollees, and perhaps that’s generally true. The influx in HealthCare.gov states may have had an impact on this front.

It’s clear in any case that HealthCare.gov states are trending in the wrong direction with respect to CSR takeup, and the question of why deserves more probing.

For detailed enrollment data for 2023 and prior years, see CMS’s marketplace public use files.

UPDATE, 3/24/23: Two proposed rule changes in CMS’s annual Notice of Benefit and Payment Parameters (NBPP) for 2024 might improve silver selection at low income levels. First, as Jason Levitis points out to me by email, and as he wrote in Part 2 of Health Affairs’ overview of the NBPP, CMS proposes allowing exchanges to auto-reenroll low-income enrollees in bronze plans in silver plans from the same network with the same insurers, as David Anderson proposed in JAMA in 2021. (See p. 28 in the NBPP: “Specifically, we propose to allow Exchanges to direct re-enrollment for CSR-eligible enrollees from a bronze QHP to a silver QHP with a lower or equivalent net premium under the same product and QHP issuer, regardless of whether the enrollee’s current plan is available.” Second, having re-introduced a set of plans with standardized benefits (swimming in a sea of nonstandard plans) on HealthCare.gov in 2023, CMS proposes limiting nonstandard plans to two per metal level and network type per insurer (i.e., two nonstandard HMOs and PPOs per metal level per insurer), as discussed in this post. A third option for HealthCare.gov would be to follow some state-based marketplaces in “defaulting to silver” — i.e., showing silver plans first — to CSR-eligible enrollees. One difficulty on this front is that doing so requires nuance — plan menus should not default to silver for enrollees in the 200-250% FPL income range, as the weak CSR available at that level (raising AV to just 73%) is often less valuable than discounts in gold and bronze plans produced by silver loading. Unfortunately, the SBEs that default to silver don’t take this change in market realities into account, as discussed in this post. (silver loading began in 2018, after Trump’s cutoff of direct CSR reimbursement)

Update 2: On Twitter, Aleka Gürel, who works at the commercial e-broker HealthSherpa (which processes more than a third of HealthCare.gov applications), emphasizes a point I touched on briefly in the post:

My 2C: network is a huge part of this. "Buying up" to the network you need on silver can cost $50-100 per month - hard to compete with $0 bronze, esp if you're a low utilizer and feel you can get by with the pre-deductible coverage.

I would add that silver loading — the pricing of the value of CSR directly into silver plans, raising both silver plan premiums and subsidies and so reducing net-of-subsidy premiums for plans that cost less than the benchmark plan — may also be contributing to the flight from silver, not only by making bronze and sometimes gold plans free in the 150-200% FPL range, but also by increasing price spreads between benchmark silver and more expensive silver plans.

Update 3: David Anderson adds in a note that another factor may be an inflation-driven spike in the Federal Poverty Level, and so in the FPL multiples that determine CSR eligibility and CSR level (as well as percentage of income required for a benchmark silver plan — “"i.e.," David writes, "someone who was 203% FPL in 2022 with Gold is now 196 FPL and automatically re-enrolled back into Gold this year."

Update 4: Re forgoing high-CSR silver to get access to a valued insurer/provider network: Recalling now that in a post last March I explored one specific example:

One potential motive [for forgoing high-CSR silver] was suggested to me by Cynthia Cox, ACA program director at the Kaiser Family Foundation: Silver plans from Kaiser Permanente, probably the nation's foremost provider-run HMO and the state's dominant insurer, with 34% market share among new enrollees in 2022, are priced well above those of the lowest-cost insurers in much of the state. In LA County, at an income of $19,000 (slightly under 150% FPL), silver plans from L.A. Care and Anthem are available for free, while the Kaiser silver plan costs $46 per month for a single 40 year-old.** While 21.5% of Anthem's enrollees obtained the highest level of CSR and so had incomes below 150% FPL, just 9% of Kaiser enrollees did. Some low-income enrollees may choose bronze plans to get free or lower-cost access to Kaiser or more expensive plans (e.g., broader-network PPOs) offered by other insurers.

No comments:

Post a Comment