Note: All xpostfactoid subscriptions are now through Substack alone (still free), though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up!

|

| Texas, our largest Medicaid desert |

While the 2023 Open Enrollment Period for the ACA marketplace was a success in bringing more people into coverage (total enrollment increased 12.7% nationally), my last post focused on one way in which the marketplace degraded: A lower percentage of low-income enrollees selected silver plans than in 2022, thereby forgoing the Cost Sharing Reduction (CSR) subsidies that raise silver plan value to a roughly platinum level at incomes up to 200% of the Federal Poverty Level*. CSR is available only with silver plans. In HealthCare.gov states, silver plan selection was at its lowest level ever in 2023 at incomes up to 150% FPL, and at its second-lowest level ever at incomes in the 150-200% FPL range*.

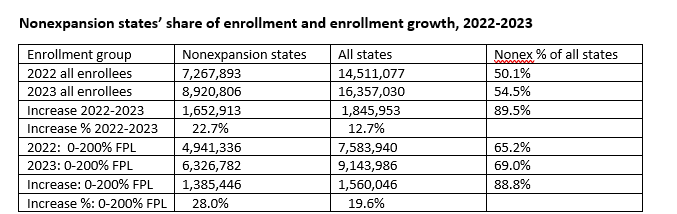

Since enrollment at low incomes is heavily concentrated in the twelve states that had not enacted the ACA Medicaid expansion as of OEP for 2023 (Nov. 1 - Jan. 15), here I want to look at the drop in CSR takeup in those twelve states. In nonexpansion states, eligibility for marketplace subsidies begins at 100% FPL, as opposed to 138% FPL in expansion states, where Medicaid is available below that threshold. The need for coverage at low income levels in nonexpansion states is particularly desperate, as those who estimate income below 100% FPL get no help at all. Enrollment in the twelve current nonexpansion states in the lowest subsidy-eligible income cohort, 100-150% FPL, has surged from 2.8 million in 2021 to 4.8 million this year.

In nonexpansion states, after a surge in low-income enrollment in 2023, 55% of enrollees have incomes under 150% FPL, qualifying them for a free benchmark silver plan enhanced by Cost Sharing Reduction (CSR), which at that income level reduces the median deductible to $0 and the mean deductible to $49 (see CMS’s Public Use File for plan design, 2014-2023). In 2023, 18% of enrollees in this income cohort — about a million enrollees — selected bronze plans, with median deductibles of $7,200 (though an increasingly sizable percentage of bronze plans sport $0 medical deductibles, albeit with drug deductibles average $3,800 and inpatient hospital copays of $3,000).

The metal level choices of low-income enrollees in nonexpansion states are not appreciably different from those for all HealthCare.gov states, or for all 51 states (including D.C.). That’s in large part because the vast majority of low income enrollees are concentrated in the nonexpansion states. In fact, 79% of all enrollees with income under 150% FPL nationally are in nonexpansion states, and 69% of enrollees with income below 200% FPL. Enrollment growth in the two years since the American Rescue Plan Act massively boosted ACA premium subsidies is also overwhelmingly concentrated in the nonexpansion states. (CMS Public Use Files* for the marketplace are the source for both tables below.) The nonexpansion states’ share of national marketplace enrollment grew in 2023.

Source: CMS Public Use Files for the marketplace (both tables)

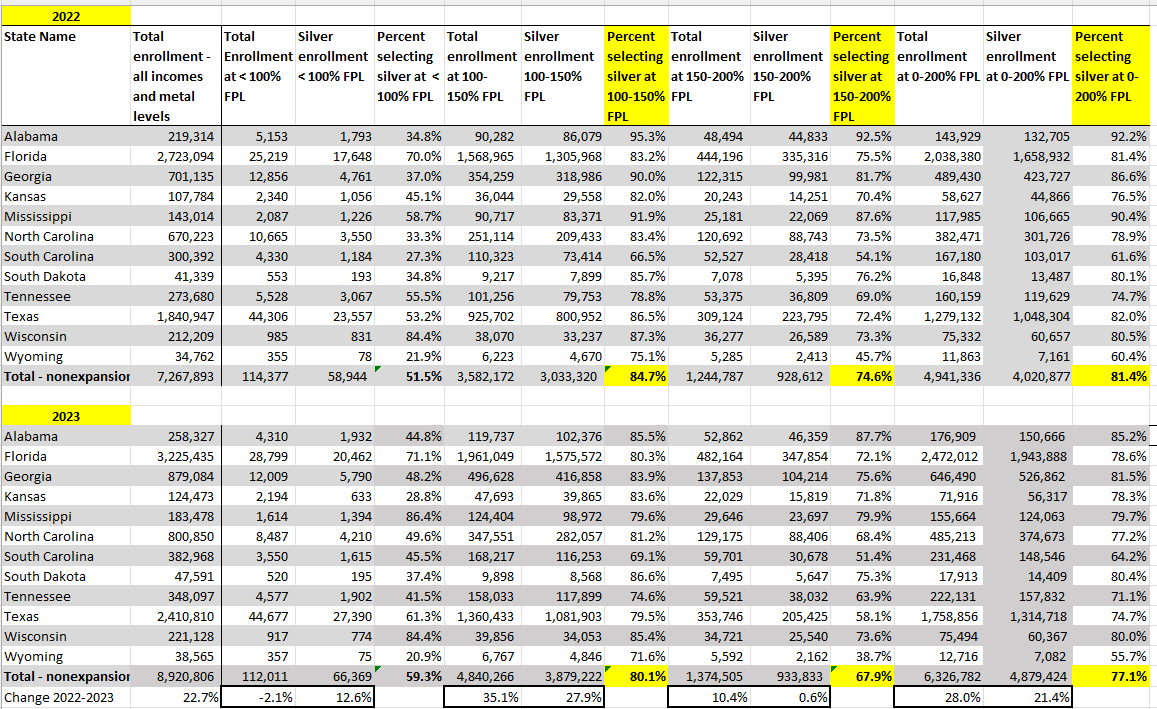

In short, the nonexpansion states are where the rubber meets the road for CSR. The chart below (click to expand) illustrates the drop in silver plan selection in those states from OEP 2022 to OEP 2022.

Silver Plan Selection at Low Incomes in Nonexpansion States, 2022-2023

About 1.4 million enrollees in these states who qualify for high-CSR silver plans with actuarial values of 94% (for incomes up to 150% FPL) or 87% (at 150-200% FPL) aren’t getting them, and the vast majority of those who forgo silver are enrolled in bronze plans.

The bottom row highlights the extent to which enrollment growth in the two main income brackets spotlighted here (100-150% FPL and 150-200% FPL) outstripped silver enrollment growth in those brackets. Silver enrollment conversely spiked at income below 100% FPL, but that is a very small category.

In my last post, I mentioned that some enrollees may have good reasons to forgo CSR silver — chiefly, if the silver plans provided by an insurer with a provider network that suits their needs is priced significantly above the benchmark (second cheapest) silver plan. In some cases, most notably in Texas in 2023, gold plans are priced below silver and may be a viable option, particularly in the 150-200% FPL income bracket, if a silver plan from a desired insurer is too expensive. Updates at the foot of the last post address factors that may induce low-income enrollees to choose bronze or plans, with interesting input from informed readers (mostly via Twitter).

A few further notes:

- Legally present noncitizens who are subject to a federal “five-year bar” to Medicaid eligibility, or laws in some states requiring a longer wait period, are eligible for premium subsidies even if their income is below the 100% FPL eligibility threshold that applies to citizens. Low silver plan selection among the small number of enrollees with income below 100% FPL indicates that a significant number of enrollees in this category are not subsidy eligible, i.e., are not legally present noncitizens.

- About 1% of silver plan enrollees (44,000) with income below 150% FPL do not receive CSR. Many-to-most of them may be among the 66,000 silver plan enrollees with income below 100% FPL, but CMS does not break out “CSR 94” enrollees by income (0-100% or 100-150% FPL).

- CMS breaks out metal level selection by income via a rounded percentage for each income bracket of the total enrollment in a given metal level. I convert that rounded percentage into an enrollment total, so those totals are estimates. (For example, the table shows 60% of 200,000 all silver plan enrollees for a state in the 100-150% FPL bracket, I would list 120,000 silver enrollees in that bracket.)

I’ll conclude with a friendly reminder that about 4.2 million marketplace enrollees in HealthCare.gov states have income below 138% FPL, and almost all of them would be in Medicaid if the remaining ten holdout states (South Dakota and North Carolina will expand Medicaid within a year) were to enact the expansion.

—-

* A weak form of CSR, raising actuarial value just three points to 73%, is available to enrollees in the 200-250% FPL income bracket. Silver plan selection in that bracket has quite rationally fallen off a cliff since the silver loading era began in 2018. See this post for more.

Photo by Yigithan Bal.

No comments:

Post a Comment