Subscribe (free) to xpostfactoid

An ASPE brief released by HHS today, highlighting the relatively low out-of-pocket costs available to low-income ACA marketplace enrollees who enroll in silver plans with Cost Sharing Reduction (CSR) subsidies, centers on a rather strange claim:

Median and average deductibles, after CSRs, differ substantially among HealthCare.gov enrollees. The median deductible decreased from $1,000 to $750 between 2017 and 2021 (prior to implementation of the American Rescue Plan (ARP), while the average deductible increased from $2,405 to $2,825. The difference between median and average deductibles is primarily driven by the fact that the majority of enrollees are eligible for and select CSR-silver plans; the average deductible is driven up by the smaller share of enrollees enrolled in plans without CSRs.

Why is there now a "smaller share of enrollees enrolled in plans without CSRs"? It's not because low income enrollees selected silver plans at a higher rate in 2021 than in 2017 - - the opposite is true. Let's dig in.

1. Why did the median deductible go down while the average deductible went up? The average deductibles for CSR plans with an AV of 94% (CSR94) and 87% (CSR87) did go down a bit, while average silver plan deductibles at other income levels rose, as did gold and platinum deductibles. For CSR87, the average went down from $661 in 2017 to $530 in 2021, according to the ASPE brief. But total enrollment in CSR94 and CSR87 plans does not quite reach the median in any year.

2. Enrollment in recent years has surged in states that have refused to enact the ACA Medicaid expansion, and in those states, eligibility for marketplace subsidies begins at 100% FPL, rather than 138% FPL (the Medicaid eligibility threshold) in expansion states. Enrollment in nonexpansion states increased by 10% from 2020 to 2021, and by 17% at incomes that qualify for the highest level of CSR (100-150% FPL). The percentage of enrollees in HealthCare.gov states with incomes in this range has accordingly risen from 35% in 2017 to 41% in 2021. At, the three states that exited the federal marketplace in this time period -- Nevada, New Jersey, and Pennsylvania -- have all expanded Medicaid. Their exit increases the concentration of low income enrollees in states using HealthCare.gov (though Kentucky, which rejoined the federal exchange in 2017, also has expanded Medicaid).

2. Low income enrollees' selection of silver plans, which entitles them to CSR, deteriorated at every CSR-eligible income level from 2017 to 2021, but at highly variable rates. Silver plan selection collapsed at 200-250% FPL, where CSR is negligible, from 68% in 2017 to 33% in 2021 ; sank from 83% to 67% at 150-200% FPL in the same time period; and remained relatively stable at 100-150% FPL, dropping from 89% to 83%* (also see charts in this post). In 2018**, 14% of all CSR enrollees in HealthCare.gov states had incomes in the 200-250% FPL range and so obtained the lowest level of CSR. In 2021 just 8% of CSR enrollees were in that category. Conversely, in 2018 56% of CSR enrollees obtained the highest level of CSR, and that percentage rose to 66% in 2021.

3. That shift in the income distribution of CSR enrollees (and so in the level of CSR they obtain) partly offset the deterioration in CSR takeup. The percentage of enrollees who obtained the two highest levels of CSR (CSR with AVs of 94% or 87%) was all but identical in 2018 (46.5%) and 2021 (46.3%).

4. The comparison above is between 2018 and 2021 because in 2017, CMS did not break out CSR enrollment by different AV levels. A near proxy for CSR94/CSR87 enrollment, however, is the percentage of enrollees with incomes in the 100-200% FPL range who selected silver plans (it's inexact because a) about 2-3% of enrollees have incomes below 100% FPL, at which level legally present noncitizens time-barred from Medicaid are subsidy-eligible), and b) some enrollees at 100-200% FPL are not subsidized and so don't obtain CSR). In 2017, 49.7% of all enrollees in HealthCare.gov states were silver plan enrollees with incomes the 100-200% FPL range, compared to 47.4% in 2018. The percentage of enrollees in CSR94/87 in 2018 was about one percentage point lower than silver enrollees at 100-200% FPL -- suggesting that in 2017, almost 49% of enrollees in HealthCare.gov states obtained CSR94/87. All the stranger, then, that median deductibles went down so dramatically. But many CSR87 enrollees are in plans with deductibles well above the median, so CSR94/87 enrollment is not the whole story.

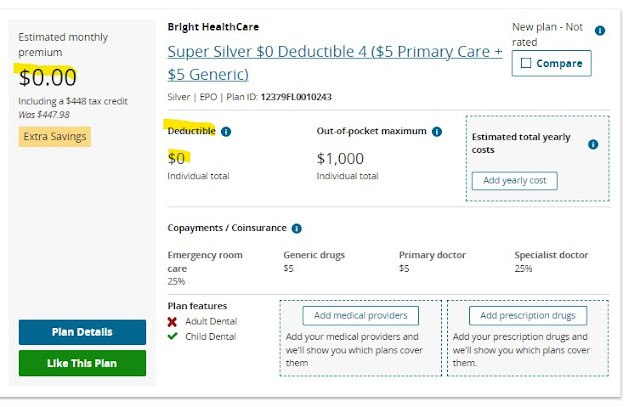

5. So why did median deductibles go down? A smattering of low deductible plans at other income levels (there are even $0 deductible bronze plans****) must have pushed the percentage of enrollees with deductibles under $750 over 50%. A three percentage point increase in gold enrollment from 2017-2021 may have helped: though most gold plans have deductibles well above $750, some don't (and in 2017 as in 2021, there were enough gold plan enrollees to push the percentage of enrollees who obtained 80% AV (the gold AV) or higher over 50%). Notably, average bronze plan deductibles declined in 2020 and 2021, perhaps pushed down in part by the advent of $0-deductible bronze plans offered by some cut-rate insurers, e.g., by Bright Health Care in Texas. (That bronze plans, with an AV of 60%, can post $0 deductibles underscores that the deductible itself is a limited indicator of out-of-pocket costs.)

6. I have to say I don't know why the median deductible in HealthCare.gov states was lower in 2021 than in 2017. The 50% cut point remains hidden: I would guess that the smattering of low deductible plans at metal levels other than CSR94/87 pushed the median to somewhere near the upper end of CSR87 deductibles, which had a median of just $450 in 2021 but can go as high as $2,000.

The ASPE brief obscures the picture a bit with this bullet point:

Slightly over half of HealthCare.gov enrollees – 51 percent in the 2021 open enrollment period and 58 percent of new plan selections during the 2021 special enrollment period (from February to August) –receive CSRs, making a CSR plan the median HealthCare.gov offering. The average silver CSR deductible, after subsidy, has been well below $1,000 for the past 5 years, and is even lower for those with incomes below 200 percent of the federal poverty level who qualify for more generous CSRs.

"Average silver CSR deductibles" are neither here nor there, as at the 73% AV level CSR deductibles average $3,385, per KFF. This brief is focused on the median.

An elephant in this room, not discussed at all in the ASPE brief, is silver loading, a pricing practice that began in 2018. In October 2017, Trump cut off direct reimbursement of insurers for the value of CSR, which was required by statute but never funded by a (Republican) Congress. Regulators in almost all states responded by allowing or encouraging insurers to price the value of CSR into premiums for silver plans only, since CSR is available only with silver plans. Since ACA marketplace subsidies are designed so that the enrollee pays a fixed percentage of income for the benchmark (second cheapest) silver plan, the result was discounts in bronze and gold plans. Free bronze plans became widely available at low incomes, and gold plan selection roughly doubled, from 4% to 8% nationally (though gold plan premiums did not sink as much as forecast). Silver plan selection collapsed at incomes above 200% FPL, the threshold for strong CSR (including at 200-250% FPL, where weak CSR is available), and eroded at lower incomes as well. Silver loading probably increased average deductibles obtained by enrollees, as it pushed many more enrollees into bronze plans, but by boosting gold plans it may have pushed down the median.

The ARP reversed the erosion of silver selection at low incomes, by making silver plans free to enrollees with incomes up to 150% FPL and costing a maximum of just 2% of income in the 150-200% FPL range ($43 per month for an individual at 200% FPL in 2022, as opposed to about $135/month pre-ARP). Accordingly, during the emergency Special Enrollment Period that ran for much of 2021, silver selection at low incomes recovered from its four-year slide, probably reaching about 90% at incomes up to 200% FPL and near 95% at incomes up to 150% FPL, where high-CSR silver is free. We will find out in March or April, when CMS releases public use files for the 2022 Open Enrollment Period, whether that high CSR takeup continued during OEP -- or possibly even increased, as the Biden administration ramped up federally funded enrollment assistance.

If CMS wants to further reduce enrollees' out-of-pocket costs, it could require insurers to price gold plans below the silver plans, as 5 states have effectively done (one, New Mexico, has required insurers to price silver at a platinum level, as high-CSR silver plans are rough platinum equivalents). On average, thanks to CSR, silver plans have a higher actuarial value than gold plans. Analysts (including CBO) that gamed out the likely effects of silver loading before Trump's long-anticipated CSR reimbursement cutoff expected gold plans premiums to drop below those of silver plans. That's happened only in spots. Insurers compete to offer the lowest-cost silver plans, since those plans still dominate the market. Moreover, the risk adjustment formula that CMS uses to compensate plans that attract higher-cost enrollees is said by many analysts to favor silver plans. CMS might need to adjust that formula as prelude to requiring insurers to price plans in strict proportion to their average actuarial value (average, because AV varies by income in silver plans).

Finally, if CMS really wants to reduce out-of-pocket costs, it can change the formula for calculating actuarial value by eliminating the highest-risk enrollees, whose costs skew the averages, from the calculation. That would raise effective AV at each statutorily-determined metal level and CSR level. The AV formula was not handed down from Mount Olympus.

P.S. I do think that the high-AV coverage obtained by about half of marketplace enrollees deserves occasional emphasis.

--

* Enrollment stats are derived from CMS's public use files for marketplace enrollment in 2017, 2018 and 2021 unless otherwise indicated.

** In 2017, CMS did not break out CSR enrollment at the different AV levels, as discussed

*** Correction, 1/14/21: I initially thought that the percentage of enrollees with strong CSR had increased from 2018 to 2021, not recognizing that the decline in CSR takeup fully offset the downward shift in median income. This paragraph has been rewritten accordingly, and point #4 added.

**** Plans can be tricky with deductibles. A plan may have a $0 deductible and a $3000 copay for hospital admission. Or it may have a $0 deductible in a narrow Tier 1 and a $6000 deductible in higher tiers.

No comments:

Post a Comment