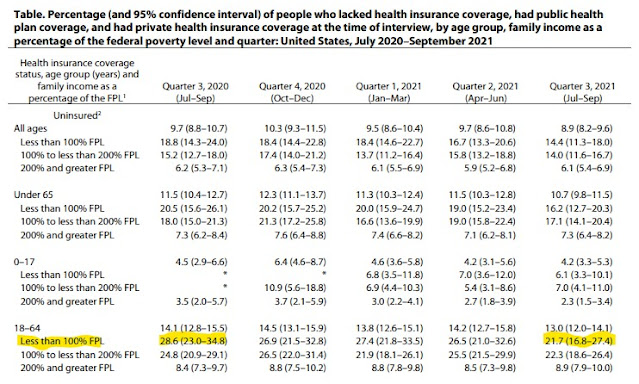

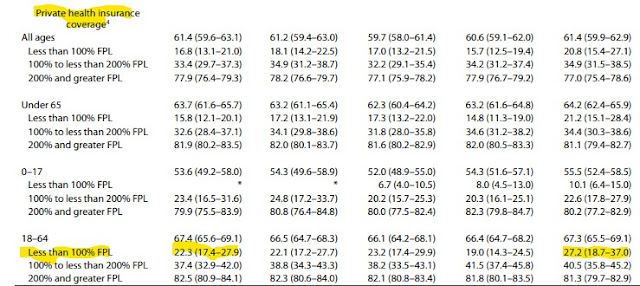

The latest quarterly estimates of health insurance coverage from the National Health Interview Survey (NHIS) show a drop in the uninsured rate for all ages from 9.7% in Q2 2021 to 8.9% in Q3. That's probably not statistically significant. The confidence intervals largely overlap; quarterly rates bounce around quite a bit; they are "published prior to final data editing and final weighting"; and response rates have been affected by the pandemic.

That said, the changes among adults aged 18-64 in the lowest income segment -- those with incomes below the Federal Poverty Level -- may be worth pausing over:

- These numbers are bouncy -- why the drop in Q2 2021?

- Most private health insurance is via employer-sponsored plans. And the unemployment rate dropped from 5.9% at the end of Q2 to 5.1% at the end of Q3. But employment-sponsored insurance is rare for people with incomes below 100% FPL. And private insurance at higher incomes dropped slightly or remained flat.

- In surveys, people who are enrolled in managed Medicaid plans, which are branded by the commercial insurers that provide them, sometimes identify their coverage as "private." And Medicaid enrollment surged throughout the pandemic -- while the percentage of people under 100% FPL reporting enrollment in "public health insurance" dipped 3.8 percentages point from Q2 to Q3 2021.

- ACA marketplace subsidies are (theoretically) not available to people in households with income below 100% FPL. And marketplace subsidies are determined by an estimate of future income -- which, as outlined below, may have been stimulated upward by various pandemic developments. Moreover, the NHIS defines a household as "everyone who usually lives or stays in the household," whereas the marketplace defines a household as everyone filed under one tax return. The same income for a larger household has a lower FPL.

All that said...the pandemic has coincided with a major enrollment surge in the ACA marketplace in states that have not enacted the ACA Medicaid expansion . From the end of the Open Enrollment Period for 2020 (Dec. 15, 2019) to the end of OEP for 2022 (Jan. 15, 2022), enrollment growth in the 12 remaining nonexpansion states will likely scrape 40%. That's an increase of close to two million (1.8 million as of Dec. 15*). In the nonexpansion states, more than 40% of enrollees have incomes that would qualify them for Medicaid had their states enacted the expansion -- that is, below 138% FPL, the eligibility threshold established by the expansion.

I have wondered whether the pandemic both incentivized and enabled a significant number of people formerly in the coverage gap to climb out by reporting/estimating incomes over 100% FPL. Government actions that helped in this regard include the large supplemental unemployment insurance granted in 2020 by the CARES Act; the provision in the American Rescue Plan deeming anyone who received any unemployment insurance income in 2021 eligible for free benchmark silver coverage; a rule implemented in May 2021 that stopped the exchanges from requiring income verification from people who claimed an income over 100% FPL (the eligibility threshold) if "trusted sources" indicate that their income is lower; and a major surge in federally funded enrollment assistance (assistors can help applicants make sure they consider all income sources). The newly effective rule essentially granting year-round enrollment to anyone reporting an income below 150% FPL should help further, as any income boost may enable an applicant to estimate an annual income above the required threshold.

* The 37% two-year increase for nonexpansion states cited in the post at the link includes Wisconsin, which has not enacted the ACA expansion but does cover adults with incomes up to 100% FPL (as opposed to 138% FPL, the ACA standard), and so has no coverage gap (eligibility for marketplace subsidies begins at 100% FPL, as in all nonexpansion states). Excluding Wisconsin, which lacks the "marketplace or nothing" enrollment incentive, raises the increase by about a percentage point.

No comments:

Post a Comment