My festschrift contribution for Kevin Drum, who's recovering from a stem cell transplant in treatment for multiple myeloma, is up on Mother Jones. Kevin, give thanks, is doing very well, and managing to keep blogging on policy as well as track his treatment experience.

For those interested in the editing process -- as anyone who's ever edited inevitably is -- I thought my piece was skillfully shaped by Mother Jones managing editor Clint Hedler. Mostly he cut caveats and qualifications, which I've highlighted in the full draft below. Left to my own devices, I would leave the first and last highlighted sections in place and let the other cuts stand -- and I can see the case for all of them. I should be better at doing this to myself, as I spend half my day-job hours doing it to other people's articles.

---------------

One thing I've always appreciated about Kevin is that his commitment to economic justice is grounded in political realism. That balance was on display in his postmortem on the Democrats' drubbing in November:

The Affordable Care Act is a really stark exemplar of the good policy/tough politics conundrum. For almost its entire life its approval ratings have been underwater -- though just this week, as Kevin noted, it crept into positive territory in the Kaiser Family Foundation's tracking poll for the first time since November 2012, when it basked briefly in the glow of its newly re-elected namesake. Even now, more people say the law has hurt than harmed them, though the majority say it hasn't affected them directly.

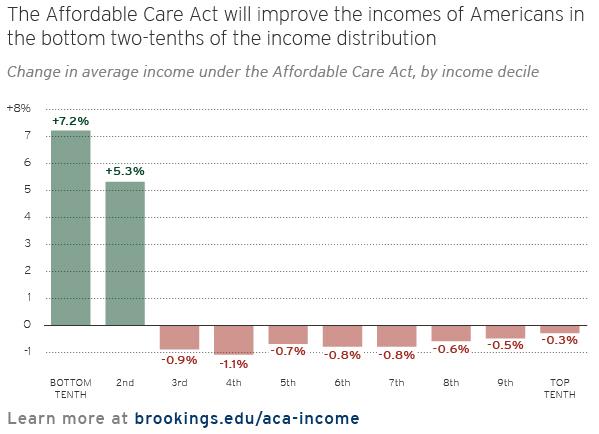

Most of the ACA's supporters assume that the ACA has remained unpopular because, as Jonathan Chait put it, "[Republicans'] lies got halfway around the world before the truth could get its pants on. And that's largely true. But it's also true that the law's impact on Americans' incomes look something like this:

That chart is a simplified takeaway from a study of the ACA's likely effects on income by Brookings economists Henry Aaron and Gary Burtless*. In fact it's a very simplified takeaway: the authors define income four different ways; they acknowledge that insurance is particularly difficult to value, and they necessarily leave out key factors such as the law's possible effects on healthcare spending growth, which has slowed dramatically in the years since the ACA was passed (though the degree to which the ACA has contributed to that slowdown, if at all, is unclear). But the chart does starkly illustrate whom the ACA spends money on -- via premium subsidies and Medicaid benefits. It's the bottom 20 percent of the income distribution.

Recent ACA enrollment data bears this out. Of the 11.7 million buyers of private health plans on the ACA exchanges, over 60% have incomes under 200 percent of the Federal Poverty Level (FPL) The 11 million beneficiaries of the Medicaid expansion all have incomes under 138 percent FPL. In sum, about 80 percent of the law's direct beneficiaries have incomes below 200 percent FPL. According to the Kaiser Family Foundation, 34 percent of Americans and 57 percent of the pre-ACA uninsured (as of 2013) had incomes below that level.

Sliced another way, about half (48 percent) of private plan buyers in the 37 states using healthcare.gov had incomes ranging from 150-300 percent FPL, a more or less working class range. But more than half of those were at the lower end, 150-200 percent FPL.

The truth is, the ACA private plan market works best for people with incomes under 200 percent FPL That's the cutoff point for really strong Cost Sharing Reduction subsidies that make the coverage comparable to (or, for those under 150 percent FPL, better than) that offered by high-quality employer-sponsored policies. A recent study by Avalere Health showed that takeup rates for private plans offered on ACA exchanges are sky-high among the lowest-income uninsured who qualify for subsidies -- but drop like a rock for uninsured buyers at higher income levels. It would be great if more generous subsidies could make the exchange plans more attractive to those on the upper end of the subsidy scale, but Democrats allocated what the political traffic would bear.

So how do the ACA's offerings to the uninsured affect the working class, white or otherwise? For starters, 200 percent FPL, the upper end of the sweet spot for ACA benefits, is a working class income; it's just under $40,000 for a family of three, and about two-thirds of median income. As noted above, 34 percent of Americans have incomes below that threshold.

But income in the U.S. is volatile. According to the economist Stephen J. Rose, in 2010, 7-8 percent of working-age U.S. adults were below the poverty line, but in the five years prior, about 18 percent spent at least one year in poverty. The same ratio may not hold for the 200 percent FPL level, but it seems fair to assume that half of U.S. households will fall below it at some point in their existence.

Pre-ACA, health insurance status was also highly volatile. A 2008 study by Mathematica Policy Research found that while 17.6 percent of non-elderly U.S. adults were uninsured as of January 2001, 35 percent had been uninsured at some point over the three years prior. Of those, 60 percent went without coverage for at least a year. Extend the volatility caused by our employer-based health insurance system over a lifetime, and a very large percentage of Americans are likely to need an affordable fallback at some point.

There's much more to be said (and studied) about how the ACA affects the working class and indeed all of us. The law will have multiple positive and negative impacts on employer-sponsored insurance, on the way care is organized and paid for, on hospital consolidation, Medicare, etc. etc. Republicans will continue to trumpet every real and perceived negative effect (such as pending employer cutbacks to the most generous plans, which will be subject to a so-called Cadillac Tax as of 2018).

In the longest view, if the ACA really is contributing to a long-term slowdown in the growth of US healthcare spending -- admittedly a big 'if' though the data is promising -- it could secure the nation's fiscal future. As Peter Orzag kept telling us back in 2009, "healthcare reform is entitlement reform" -- a genuine long-term bend in the healthcare cost curve would be worth all the Bowles-Simpson-type spending cut/tax hike plans ever conceived. Democrats may never see any long-term electoral benefit from that scenario if it unfolds -- and if it does, it will probably be genuinely difficult to untangle the ACA's effects from those of future reforms triggered by both its successes and its failures.

At the same time, the ACA has already cut the ranks of the uninsured by 15 million, reducing the uninsured rate among non-elderly adults from 17.6 percent to 10.1 percent, as estimated in a just-published Urban Institute study. In states that accepted the Medicaid expansion, it's cut the uninsured rate of the poor in half. For the middle class -- very broadly defined by Urban as those in households between 138 percent and 400 percent FPL -- it's raised the insured rate by 7.6 percentage points.

That's a monumental accomplishment, and Democrats paid for it in political blood. We should honor them for that.

---

* Hat tip to Bill Gardner, who cited the Aaron/Burtless finding as a partial explanation for the ACA's lingering unpopularity here.

For those interested in the editing process -- as anyone who's ever edited inevitably is -- I thought my piece was skillfully shaped by Mother Jones managing editor Clint Hedler. Mostly he cut caveats and qualifications, which I've highlighted in the full draft below. Left to my own devices, I would leave the first and last highlighted sections in place and let the other cuts stand -- and I can see the case for all of them. I should be better at doing this to myself, as I spend half my day-job hours doing it to other people's articles.

---------------

One thing I've always appreciated about Kevin is that his commitment to economic justice is grounded in political realism. That balance was on display in his postmortem on the Democrats' drubbing in November:

when the economy stagnates and life gets harder, people get meaner. That's just human nature. And the economy has been stagnating for the working class for well over a decade—and then practically collapsing ever since 2008.As Kevin acknowledges, this is an age-old problem for Democrats. It's "unfair" in that there's overwhelming evidence that safety-net programs like food stamps, Medicaid and the Earned Income Tax Credit "have positive effects on health, educational attainment, earnings and employment years later," as Jared Bernstein recently wrote. Conversely, programs popular with the middle class, such as the mortgage tax credit and tax-sheltered college savings plans, bestow the bulk of their benefits on the affluent. The distinction between "the poor" and "the working class" may also be too neat, given the volatility of Americans' incomes and the erosion of stable jobs at working class pay levels. An awful lot of working people access the benefits that Kevin lists, or have family members who do, (e.g., a large majority of food stamp beneficiaries). All that said, the perception that Kevin fingers is a political force, and partly grounded in reality, in that safety net programs (for the non-elderly at least) do most directly benefit those at the bottom of the income distribution.

So who does the WWC [white working class] take out its anger on? Largely, the answer is the poor. In particular, the undeserving poor. Liberals may hate this distinction, but it doesn't matter if we hate it. Lots of ordinary people make this distinction as a matter of simple common sense, and the WWC makes it more than any. That's because they're closer to it. For them, the poor aren't merely a set of statistics or a cause to be championed. They're the folks next door who don't do a lick of work but somehow keep getting government checks paid for by their tax dollars. For a lot of members of the WWC, this is personal in a way it just isn't for the kind of people who read this blog.

And who is it that's responsible for this infuriating flow of government money to the shiftless? Democrats. We fight to save food stamps. We fight for WIC. We fight for Medicaid expansion. We fight for Obamacare. We fight to move poor families into nearby housing.

This is a big problem because these are all things that benefit the poor but barely touch the working class.

The Affordable Care Act is a really stark exemplar of the good policy/tough politics conundrum. For almost its entire life its approval ratings have been underwater -- though just this week, as Kevin noted, it crept into positive territory in the Kaiser Family Foundation's tracking poll for the first time since November 2012, when it basked briefly in the glow of its newly re-elected namesake. Even now, more people say the law has hurt than harmed them, though the majority say it hasn't affected them directly.

Most of the ACA's supporters assume that the ACA has remained unpopular because, as Jonathan Chait put it, "[Republicans'] lies got halfway around the world before the truth could get its pants on. And that's largely true. But it's also true that the law's impact on Americans' incomes look something like this:

Recent ACA enrollment data bears this out. Of the 11.7 million buyers of private health plans on the ACA exchanges, over 60% have incomes under 200 percent of the Federal Poverty Level (FPL) The 11 million beneficiaries of the Medicaid expansion all have incomes under 138 percent FPL. In sum, about 80 percent of the law's direct beneficiaries have incomes below 200 percent FPL. According to the Kaiser Family Foundation, 34 percent of Americans and 57 percent of the pre-ACA uninsured (as of 2013) had incomes below that level.

Sliced another way, about half (48 percent) of private plan buyers in the 37 states using healthcare.gov had incomes ranging from 150-300 percent FPL, a more or less working class range. But more than half of those were at the lower end, 150-200 percent FPL.

But income in the U.S. is volatile. According to the economist Stephen J. Rose, in 2010, 7-8 percent of working-age U.S. adults were below the poverty line, but in the five years prior, about 18 percent spent at least one year in poverty. The same ratio may not hold for the 200 percent FPL level, but it seems fair to assume that half of U.S. households will fall below it at some point in their existence.

Pre-ACA, health insurance status was also highly volatile. A 2008 study by Mathematica Policy Research found that while 17.6 percent of non-elderly U.S. adults were uninsured as of January 2001, 35 percent had been uninsured at some point over the three years prior. Of those, 60 percent went without coverage for at least a year. Extend the volatility caused by our employer-based health insurance system over a lifetime, and a very large percentage of Americans are likely to need an affordable fallback at some point.

There's much more to be said (and studied) about how the ACA affects the working class and indeed all of us. The law will have multiple positive and negative impacts on employer-sponsored insurance, on the way care is organized and paid for, on hospital consolidation, Medicare, etc. etc. Republicans will continue to trumpet every real and perceived negative effect (such as pending employer cutbacks to the most generous plans, which will be subject to a so-called Cadillac Tax as of 2018).

In the longest view, if the ACA really is contributing to a long-term slowdown in the growth of US healthcare spending -- admittedly a big 'if' though the data is promising -- it could secure the nation's fiscal future. As Peter Orzag kept telling us back in 2009, "healthcare reform is entitlement reform" -- a genuine long-term bend in the healthcare cost curve would be worth all the Bowles-Simpson-type spending cut/tax hike plans ever conceived. Democrats may never see any long-term electoral benefit from that scenario if it unfolds -- and if it does, it will probably be genuinely difficult to untangle the ACA's effects from those of future reforms triggered by both its successes and its failures.

At the same time, the ACA has already cut the ranks of the uninsured by 15 million, reducing the uninsured rate among non-elderly adults from 17.6 percent to 10.1 percent, as estimated in a just-published Urban Institute study. In states that accepted the Medicaid expansion, it's cut the uninsured rate of the poor in half. For the middle class -- very broadly defined by Urban as those in households between 138 percent and 400 percent FPL -- it's raised the insured rate by 7.6 percentage points.

That's a monumental accomplishment, and Democrats paid for it in political blood. We should honor them for that.

---

* Hat tip to Bill Gardner, who cited the Aaron/Burtless finding as a partial explanation for the ACA's lingering unpopularity here.

Thanks for a fine article, but the income chart is totally bogus in my view.

ReplyDeleteIncome is cash. Insurance benefits are paid to providers. If a new enrollee in the ACA pays even $100 a month, their income has gone down by $100 a month.

The right wing makes the same error when they count Medicaid benefits as income, and say that the average poor person gets $14,000 a year.

Your motives are not as mendacious as this, but the chart is still wrong.

Bob, in the full article, Aaron and Burtless use four separate measures of the ACA's impact on income. It's true that this simplified chart from the short summary is the "broadest" measure that counts the full value of the insurance instead of its impact on income. In another measure, .the impact on income is weighted so that any cash value in excess of the recipient's basic cost of food and housing is excluded (p. 5). So you have a point. But it also makes sense to value the insurance according to what it costs, as here. The actual value to a given individual of course varies according to need for healthcare and I guess the quality and value of the healthcare actually received. See charts on pp 41-42 for alternate measures.

DeleteI do not contest the fact that subsidized health care makes the recipient better off. Hell, I am on Medicare. i am far better off with Medicare's low deductibles and $110 a month payment for Part B than I ever was when I bought my own insurance last year at age 64. If Burtless has said that the ACA makes poorer people better off, I would never have protested. I just resist the academic habit of translating benefits into income.

ReplyDelete