Note: Free xpostfactoid subscription is available on Substack alone, though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up.

|

| Your income next year may be $14,000? Can you earn a little more? |

1. Blase rhetorically conflates what he’s branded as “the great Obamacare fraud” with enrollments he deems “improper” — that is, enrollments that may show some evidence that the applicant’s estimate of next-year income has been optimized to maximize subsidies. That segue is parroted by CMS in last week’s ASPE brief:

Enrollment that is improper or fraudulent is enrollment by individuals misstating their income to gain access to free plans. Phantom enrollees are unknowingly enrolled in free plans by brokers or auto enrolled. By our estimate, improper, phantom and fraudulent enrollment peaked at 5.6 million people in 2025.

2. The allegations of outright fraud — “phantom” enrollees signed up by brokers, who have no knowledge of their enrollment or no intent to use it— are chiefly based on an analysis of CMS data on ‘enrollees without claims’ (EWOC). This analysis, which ignores the high incidence of short-term enrollment in HealthCare.gov states, driven by year-round enrollment and by the Medicaid unwinding of 2023-2024 — has been effectively rebutted by Matt Fiedler (1, 2) and others. While broker fraud may have given some boost to EWOC, true “phantom” enrollments are small percentage of the enrollments branded as “improper.” As last week’s ASPE brief notes, “In 2025, CMS canceled coverage for 250,000 people enrolled without consent and identified 200,000 unauthorized plan switches.”

3. Blase estimates that more than half of the 6.2 million “improper” enrollments he alleges are people with income below 100% FPL (the eligibility threshold for subsidized marketplace coverage) in states that have refused to enact the ACA Medicaid expansion, where most adults with income below that threshold are ineligible for Medicaid. But CMS estimates that requiring applicants to verify an an income over 100% FPL when “trusted data sources” indicate an income below that threshold will reduce enrollment by only 80,000 in HealthCare.gov states (where broker fraud is concentrated). As I wrote in the prior post, “Either that is a gross underestimate, or Blase’s claim that 3.4 million people with income under 100% FPL are obtaining subsidized marketplace coverage is a gross overestimate. Or both.” And to the extent people with income below 100% FPL are estimating optimistically and getting marketplace coverage, my response remains: good. That’s a reasonable patch on the coverage gap in nonexpansion states, which is a national disgrace.

Now let’s turn to evidence of broker (or nonprofit assister) manipulation that Blase alleges in data concerning enrollees’ metal level choice, mode of re-enrollment (active or passive), and ethnicity reporting (or lack thereof). Let’s acknowledge at the outset that brokers and assisters doubtless have helped shaped responses to the massive drop in subsidies triggered by expiration of the enhanced subsidies created by the American Rescue Plan Act (ARPA) in 2021 and funded through 2025. That’s their job. The spectrum of broker input runs from outright fraud (mostly in unauthorized plan-switching, which does not create phantom enrollments) to patient, nuanced consideration of the providers and drugs a client needs and the relative risks posed by different forms of out-of-pocket exposure. Between fraud and high-value expertise is a broad range of brokerage quality from which it’s very difficult to tease out a fixed degree “improper” manipulation.

As has been said many times, low-income peoples’ actual income is often volatile, based on uncertain working hours, tips, fees collected in self-employment, multiple jobs, and frequent job shifts, and a good-faith optimistic estimate of next-year income is not fraud.

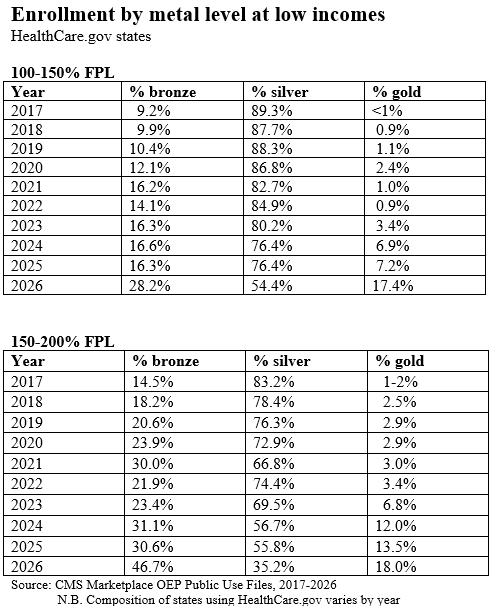

Low-income shift out of silver

For marketplace enrollees with income up to 150% FPL, Cost Sharing Reduction (CSR) increases the actuarial value of a silver plan to 94%, with deductibles averaging $172 and annual out-of-pocket maximums averaging $1,738. As Blase writes, the difference in out-of-pocket exposure between “CSR94” silver and bronze plans is enormous — and gold plans (80% AV) also substantially increase exposure, particularly in the out-of-pocket max. Yet, Blase notes, CSR takeup in the 100-150% FPL income bracket in HealthCare.gov states down-drifted throughout the Biden years — and it fell off a table in 2026. Blase writes:

The percentage of the lowest-income sign-ups enrolled in silver plans dropped precipitously between 2025 and 2026, with a much larger decline in HealthCare.gov states. The large shift away from silver plans among 100–150 percent FPL enrollees is surprising—and suspicious— because silver plans still offered dramatically better financial protection than bronze plans for only modest additional premiums. Although most silver plans were no longer fully subsidized after the expiration of the COVID-era subsidy boosts, average net premiums for many low income enrollees remained relatively modest—roughly $30–$40 per month—while the reduction in cost-sharing protection from moving into bronze coverage was enormous.

All true! At the same time, for people with income under 150% FPL ($23,475 for a single person in Plan Year 2026), a premium of $30-40/month also looms “enormous” (and the benchmark silver premium at 199% FPL tops out at $80/month). In fact, “natural experiment” studies show that even single-digit monthly premiums, compared to zero-premium, substantially reduce enrollment, as Matt Fiedler notes:

Two studies have examined this question in the Marketplaces specifically. One study examined instances in Massachusetts’ Marketplace in which an enrollee’s plan changed from having a $0 premium in one year to a $1 premium the next plan year. The authors estimate that enrollment was 12% lower among those subject to a $1 premium relative to those who remained subject to a $0 premium. Another study examined Colorado’s Marketplace and compared people just above and just below income thresholds at which enrollees lost eligibility for $0 bronze plans; the results imply that being subject to a positive premium reduced enrollment by 8-16% (depending on the precise methodology used).7

Coverage in the 100-150% FPL bracket did not drop in HealthCare.gov states in 2026 — instead, it downshifted to bronze and gold. Brokers surely facilitated this reaction, and forgoing CSR surely was not an optimal choice for everyone, but it’s not a marker of “improper” enrollment.

While the drop in silver takeup in 2026 was precipitous, it accelerated a long-term trend that predates the ARPA subsidy boost and really began with the silver loading that Trump triggered in advance of OEP 2018 by cutting off direct CSR reimbursement. Starting in 2018, insurers, to varying degrees, priced the value of CSR directly into silver plans(so-called silver loading), making zero-premium bronze coverage (and increasingly, zero-premium gold) newly available to millions. Here is how CSR takeup at the two highest CSR levels (94% and 87% AV) has trended since 2017:

Erosion in silver selection started earlier in the 150-200% FPL bracket, as pre-ARPA, a benchmark silver plan (the second cheapest silver plan in a given area) cost a single adult with an income near 200% FPL about $130/month. There is a real question, however, why silver selection at 100-150% FPL dropped about 8.5% percentage points from 2022-2024, when the two cheapest silver plans in any given rating area were zero-premium.

Increased silver loading is a big part of the answer. In 2022 the Texas legislature, following a lead from New Mexico, passed a law essentially requiring marketplace insurers to price silver plans at a platinum level (justified in the result, as the average AV obtained by silver plan enrollees in Texas is over 90%), rendering gold plans much cheaper than silver. By 2025, 25% of Texas enrollees in the 100-150% FPL bracket chose gold plans; in 2026, the percentage rose to 41%. Several other Healthcare.gov states in those years also offered gold plans priced well below silver, whether by statute, regulation or insurer choice, with three states (Arkansas, Washington and Illinois) mandating cheap silver in advance of OEP for 2026. As I’ve noted previously:

In 2018, the first year in which CSR was priced into silver plans, the lowest-cost gold plan premium averaged 109% of the benchmark silver premium, and lowest-cost gold was priced below benchmark (on average) in just 7 states. In 2026, lowest-cost gold plans are priced at 98% of benchmark silver on average, and lowest-cost gold is priced below benchmark silver in 21 states.

The growing availability of zero-premium gold plans at incomes up to 150% FPL (and beyond) explains much of the shift out of silver in 2026, as well as during the Biden years. Gold plan selection in the 100-150% FPL bracket increased by almost a million in 2026, while bronze plan enrollment increased by slightly more than a million.

Also likely contributing to reduced silver plan selection is the trend toward narrow network plans, especially at the lowest price points. Insurer participation in the marketplace increased during the Biden years, and new entrants in a given market often undercut more established players that had more robust networks. Some enrollees at least have made informed choices to forgo high-CSR silver to obtain a more robust network or formulary. I’ve interviewed brokers about this, and presented several examples of enrollees who chose lower metal level plans with eyes wide open.

When gold plans are priced well below silver plans, this downshift becomes more viable. Also on this front: in a significant number of markets, at different times, insurers have offered bronze plans with medical deductibles of zero. In 2026, 11% of bronze plans had a $0 medical deductible. As a bronze plan AV can’t top 65%, the insurer has to boost the enrollee’s out-of-pocket exposure by other means, such as with a $2,000 drug deductible or a $3,000 hospital copay.

In Houston this year, a 40 year-old with an income of $23,000 (just under 150% FPL) had a choice of two gold plans with $0 premium and a $2,000 deductible, vs. three silver plans with $0 deductible but premiums in the $70-80/month range. Network quality aside, that’s not an easy choice — notwithstanding that the out-of-pocket maximum on the gold plans was $8,200 or $9,200 vs. $1,500-2,200 for the silver plans. In fact, the sheer proliferation of plans in recent years — well over 100 to choose from in the average market, with the Trump administration poised to encourage more finely-sliced near-identical plans — has created a plethora of choices that can obscure the value of CSR.

Blase notes that the erosion of silver plan selection at low incomes was much less pronounced in the 20 state-based marketplaces, taken together. But as he acknowledges, high silver takeup at low incomes in SBMs was mainly a function of supplemental state subsidies that preserved zero-premium silver, or close to it. In California, silver selection at 138-150% FPL was 95% — a takeup rate also boosted by California’s standardized plans and weak silver loading — and also by a relatively low premium for Kaiser Permanente, highly desired for its quality provider network. In LA in 2026, Kaiser offers the third-cheapest silver plan, costing a single 40 year-old with an income of $23,000 (slightly below 150% FPL) just $20/month — compared to $41/month for the same person with an income just under 150% FPL in 2023. That kind of roll-the-dice variation can drive a lot of change in a given marketplace — and suggests deliberate choice, albeit often aided by a broker or assister.

To Blase, plan-switching to avoid premiums suggests broker manipulation. In some cases it may. But more often, it probably suggests premium aversion among people with little income to spare.

Active re-enrollment

Blase argues that an upswing in active re-enrollment in HealthCare.gov states points to brokers switching clients into zero-premium plans without their knowledge:

Along with the migration out of silver plans (discussed above)…active re-enrollment was much greater in HealthCare.gov states in the 2026 open enrollment. Active re-enrollees were 52 percent of all sign-ups in HealthCare.gov states, compared to 31 percent in SBE states and 36 percent in switcher states. This distinction is important, because active re-enrollment facilitates plan switching, including movement into fully subsidized bronze and gold plans.

This argument is going to get a bit circular. In Healthcare.gov states in 2025, 28% of re-enrollees (3.95 million out of 14.2 million) switched plans. In 2026, 40% (5.3 million out of 13.2 million) switched. That increase if 1.4 million plan-switchers strikes me as a rational response to a market in which the premium for last year’s plan in most cases increased dramatically. Brokers doubtless facilitated this switching, but it would be surprising if it didn’t happen.

As for the lower percentage of active re-enrollment in SBMs, that is a longstanding difference. Back in 2023, it struck me as suggesting a possible weakness in SBMs, as passive re-enrollment in the ACA marketplace can be dangerous, if the premium spread between your prior-year plan and the benchmark plan in the new year changes. Brokers set me straight, however: passive re-enrollment in most SBMs is not dangerous, because the SBMs provide more up-to-date and reliable price information to existing enrollees and their in advance of Open Enrollment than the federal marketplace does. As broker Sheron Sidbury explained to me then:

…the Maryland exchange sends out a renewal notice that includes a subsidy estimate and premium estimate for renewal of the enrollee’s current plan. That estimate is based on the most recent income and household information the exchange has. While the estimate’s accuracy is contingent on no personal changes by the applicant, it’s based on the new (coming-year) benchmark and plan premium...

The federal marketplace, HealthCare.gov, does not provide this information to enrollees. It sends out a renewal letter, but with no specific information as to subsidy and premium in the coming year for the enrollee’s current plan. Instead, the FFM requires insurers to send renewal letters prior to November 1 (first day of OEP), with an estimate of premium in the current year. But the insurer’s letter, while it provides the plan’s new premium (before subsidy) in the current year and an estimate of what it will cost net of subsidy, bases the subsidy estimate on the prior year’s benchmark. Thus it is nearly always inaccurate…

Enrollees who don’t report ethnicity

Blase argues that the rise in enrollees who fail to report ethnicity is evidence of high-volume phantom enrollment:

The second piece of prima facie evidence of large-scale improper enrollment is a surge in enrollees with unknown race or ethnicity with the implementation of the enhanced COVID-era subsidy boosts. In 2020, 28 percent of enrollees did not report race or ethnicity. This steadily increased to 50 percent of enrollees by 2024, a percentage where it remained after the 2025 and 2026 open enrollment periods.

The sharp increase in missing race and ethnicity information from 2020 to 2024 is difficult to explain through normal enrollment behavior and is highly consistent with fraud or improper enrollment, with rogue brokers enrolling individuals without their consent.

This argument goes back to the claim of really large-scale phantom enrollment, as opposed to enrollment with varying degrees of income massaging. The core evidence for assessing phantom enrollment is the enrollment without claims (EWOC) data, which I addressed in some detail in Part 1: once more, short-term enrollments mostly explain it. CMS estimates of unauthorized enrollments are in the hundreds of thousands, not millions.

So what of this rise in the percentage of enrollees declining to provide optional information as to ethnicity? I don’t know. As Blase notes several times, the percentage of enrollments that are broker-assisted rose by about 20 percentage points in the Biden era, from 2021 to the 2023-2026 period — and brokers as a group don’t push the question. On a message board, I queried brokers about how they handle this question. In twelve responses, six said they never ask the question, two cited language they use that actively discourages a response, and four said they ask, noting that the questions are optional.

Admittedly, the percentage increase in broker assistance isn’t enough explain the reduced response. Perhaps the huge surge in low-income enrollees does. In the states that were using Healthcare.gov in 2020, enrollment in the 100-150% FPL bracket rose from 3.0 million in OEP 2020 to 10.2 million in 2026. High percentages of low-income people have challenges with English proficiency and are often immigrants who may be wary of providing more personal information than required.

Blase’s core argument — that the number of marketplace enrollees claiming income in the 100-150% FPL bracket far exceeds Census estimates of eligible people in that income bracket — has remained essentially unchanged through three iterations. I did my best to engage it in July 2024. KFF could do better, but they don’t engage in direct rebuttals. Since then, I’ve learned a lot about broker mindset, and the very broad range of broker competence, through various industry message boards — which also document the persistence of broker fraud. The mostly fraud-free SBMs provide a clear path to shutting broker fraud without erecting the new administrative barriers for enrollees that current CMS leadership is so fond of. Instead, CMS is taking further steps to reduce enrollment and erode plan quality and choice architecture (e.g., by allowing insurers to offer more near-identical plans) while writing off the resulting enrollment decreases as fraud prevention.

No comments:

Post a Comment