Note: Free xpostfactoid subscription is available on Substack alone, though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up

|

| Heavy OOP burden |

You may have read KFF’s estimate that the average subsidized 2025 enrollee in the ACA marketplace will pay 114% more* for a benchmark silver plan in 2026, if the enhanced subsidies funded only through 2025 are allowed to expire. True!

You may also have read estimates that base (unsubsidized) premiums will rise 25% (from Charles Gaba) or 26% (from KFF). Also true!

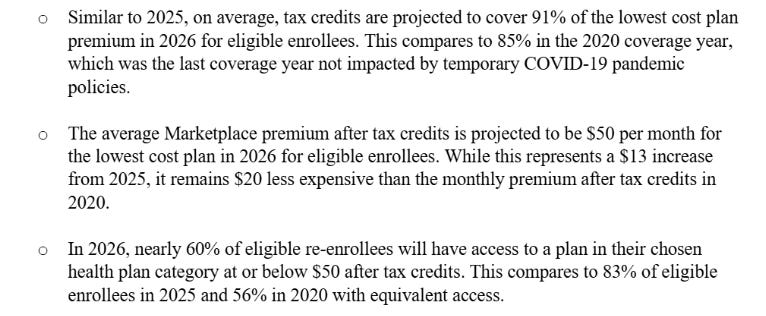

Now, as of today, you may read CMS’s proud assurance (via https://www.axios.com/2025/10/28/trump-open-enrollment-premium-prices-health-care-government-shutdownAxios) that things are not so bad:

These claims are doubtless also true! How can that be? Are premiums for subsidized enrollees going up 114% — or 35%? (i.e. from $37 to $50/month, per CMS**).

It depends, of course, on the plan you’re buying and what percentage of your actual medical claims it will cover. The KFF estimate is for the benchmark (second cheapest) plan — the one for which all subsidy-eligible enrollees pay a fixed percentage of income, which is being sharply reduced. The actuarial value of a silver plan varies with income, but for most enrollees it’s 94% or 87% (ratcheting down to 73% or 70% at income above 200% of the Federal Poverty Level (FPL).