Note: Free xpostfactoid subscription is available on Substack alone, though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up.

To fund Trump’s depraved, immoral and illegal assault on Iran, Axios reports that a Texas sage is proposing a fresh cut to ACA marketplace premiums:

House Budget Committee Chairman Jodey Arrington (R-Texas) is reviving an idea that was considered last year to fund Affordable Care Act payments known as cost-sharing reductions [CSR].

The Congressional Budget Office previously found the move would lower overall benchmark ACA premiums by 11% but result in 300,000 more uninsured people.

It would have the effect of cutting the subsidy amount that some enrollees receive, thereby increasing out-of-pocket premium costs, while saving the government over $30 billion.

That proposal would kill silver loading, which would have the most profound effects in Arrington’s Texas, where the pricing of silver plans at platinum levels mandated by statute renders gold plans far cheaper than silver plans and makes free bronze coverage available to almost all enrollees. Before Republicans in Congress seek to end the practice, the 1.7 million Texans in gold plans and likely 800,000-plus in zero-premium bronze plans might want a word.

Followers of the ACA’s 8 1/2-year silver loading saga know that “funding” CSR is a misnomer. CSR, which raises the actuarial value of a silver plan to a roughly platinum level for most silver-plan enrollees (i.e., those with income under 200% FPL), is currently funded by being priced directly into premiums — mostly into silver plan premiums, since CSR is available only with silver plans. In some states — most notably, Arrington’s Texas — this silver loading is strictly mandated by statute and regulation. (In states lacking such mandates, insurers tend to underprice silver, which remains a dominant, albeit now barely dominant, choice at low incomes.)

Silver loading began in 2018 after Trump, in October 2017, cut off the direct reimbursement of insurers for the value CSR, which is mandated by the ACA statute but was never funded by the Republican Congress (or by the Democratic Congress of 2021-22, which caught on that pricing CSR into silver plans had boosted subsidies). While Trump boasted that his abrupt move (stiffing insurers for three months’ worth of CSR in 2017, while enabling them to price it in to 2018 premiums) would kill the ACA marketplace, silver loading in fact increased premium subsidies, made free bronze plans newly available to millions, and gave the market an enrollment boost estimated at 5% in 2019. That’s because the ACA’s income-adjusted subsidies are set to a silver benchmark. When silver plan premiums rise, so do subsidies, rendering plans that cost less than the benchmark silver plan relatively cheaper for subsidized enrollees. (Plans priced below benchmark include one silver plan, most bronze plans, and, in some states and regions, some gold plans. )

In Texas, incredibly enough, the legislature in 2022 unanimously approved legislation, signed by Governor Abbot, requiring ACA marketplace insurers (as fleshed out by regulation) to price silver plans at platinum levels, on the assumption that virtually everyone who enrolls in a silver plan will have an income under 200% FPL and so obtain platinum level coverage (CSR raises the actuarial value of a silver plan to 94% at incomes up to 150% FPL and to 87% at incomes from 150-200% FPL, compared to 90% for platinum). And in fact that assumption has been borne out: in 2026, only 1% of silver plan enrollees in Texas have income over 200% FPL (78% of all enrollees in the state have income below 200% FPL). The average lowest-cost gold premium in Texas is $570/month, vs. a $671 average for lowest-cost silver. Also as a result of silver loading, which inflates silver premiums and therefore increases subsidies (which are set to a silver benchmark), bronze plans are available for zero premium to most enrollees.

How does this play out? In Houston, a single 43 year-old with an income of $31,000 — just under 200% FPL — can choose between seven free bronze plans. The cheapest available silver plan will cost her $161 per month — whereas the lowest-cost gold plan is available for just $72 per month.

Cheap gold in the marketplace is not an entirely unmixed blessing, as CSR-enhanced silver plans protect low-income enrollees from high out-of-pocket costs far more than gold plans do. For the Houston resident described above, the lowest-cost silver plan has a deductible of $800 and an annual out-of-pocket maximum of $3,000, compared to a $2,000 deductible and $9,200 OOP max for the lowest-cost gold plan. At an income of $23,000, slightly under 150% FPL, that lowest-cost silver plan has a $0 deductible and an OOP max of $1,600 — but a premium of $70/month, vs. $0/month for lowest-cost gold.

Nonetheless, strict silver loading seems pretty clearly to have mitigated enrollment loss in Texas. Nationally, ACA marketplace enrollment in 2026 was down 4.9% from 2025; in Texas, enrollment increased by 5.2%. In the 150-200% FPL range in particular, cheap gold and free bronze may have kept a lot of people in the market.

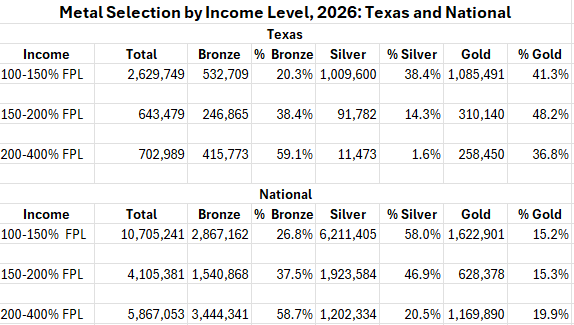

Here is a breakout of metal level selection by subsidy-eligible income brackets (with 200-400% FPL combined), in Texas and nationally, As noted in my last post, CSR takeup (silver selection at low incomes) dropped sharply nationwide, accelerating a years-long trend. Increase gold selection partly offset the move away from silver — and Texas accounts for outsized share of that shift. Texas accounts for 43.4% of all gold plan enrollment nationally, compared to 18.0% of all enrollment.

Sources: 2026 OEP State-Level Public Use File (ZIP) and 2026 OEP State, Metal Level, and Enrollment Status Public Use File

In Texas, while cheap gold plainly pulled a lot of low-income enrollees out of CSR-enhanced silver, it also likely reduced the percentage of such enrollees shifting into bronze, as bronze selection at 100-150% FPL in Texas was just 20.3%, compare to 26.8% nationally. At incomes over 200% FPL, silver in Texas became effectively a non-option, as gold is both cheaper and has a higher actuarial value — i.e., it “dominates” silver. Again, in Texas, the vast majority of enrollees had a free bronze option — e.g., a Houston 50 year-old with an annual income of $40,000, a bit over 250% FPL.

Despite the steep discount in gold in Texas, expiration of the enhanced premium subsidies created by the American Rescue Plan Act still rendered gold plans too expensive for a large share of higher-income enrollees, compared to 2025. In the 200-400% FPL income range, gold plan selection dropped from 56.3% in 2025 to 36.8% in 2026. Bronze took up the slack.

All told, you’d think at least a handful of Texas’s 38 House reps might want to have a word with Arrington —as might the cosponsors of the 2022 silver loading law, TXSenator Nathan Johnson (D) and Rep. Tom Oliverson (R).

There is a lot more to be said about metal level selection nationally — e.g., about low CS R takeup at incomes up to 150% FPL in the wake of expiration of the enhanced premium subsidies. But that’s for another post.

For a full account of the silver loading saga, see the “CSR cutoff” section of this post.

Update: Oy, this post needed some proofreading, now done. Rush rush rush. Sorry!

Public domain image here.

No comments:

Post a Comment