Note: All xpostfactoid subscriptions are now through Substack alone (still free), though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up.

This post is Part 3 of an assessment of Trump administration policy with respect to the ACA, most specifically the ACA marketplace. Part 1 overviewed the administration’s early encouragement of state reinsurance programs, Trump’s cutoff of direct reimbursement of insurers for Cost Sharing Reduction subsidies, and the defunding of the Navigator enrollment assister program, paired with considerable support for health insurance brokers.

Part 2 reviewed the effective repeal of the individual mandate penalty, paired with regulations designed to boost an alternative market of ACA-noncompliant plans. Here, we’ll look at how Seema Verma’s CMS loosened rules for insurers and tightened them for marketplace applicants.

Marketplace regulation.

In comments accompanying their various regulatory actions in the ACA marketplace, Trump officials expressed contempt and hostility for the marketplace as they inherited it — as well as solicitous intent to keep insurers aboard.

When finalizing a “market stabilization” rule in April 2017, CMS stated, reasonably enough:

Robust issuer participation in the individual and small group markets is critical for ensuring consumers have access to affordable, quality coverage, and have real choice in coverage. Continued uncertainty around the future of the markets and concerns regarding the risk pools are two of the primary reasons issuer participation in some areas around the country has been limited. The changes in this rule are intended to promote issuer participation in these markets and to address concerns raised by issuers, States, and consumers. We believe these changes will result in broader choices and more affordable coverage.

Ironically, the imperative to mollify insurers at this point was largely triggered by the Republican Congress’s effort to “repeal and replace” the ACA’s core programs, including the marketplace, and by the looming threat that Trump would stiff insurers by cutting off direct CSR reimbursement in mid plan year (the market correction and enrollment contraction of 2017 also played a role). The rule stabilization rule effected an industry wish list of tweaks, including

A shortened Open Enrollment Period (aimed at “reducing opportunities for adverse selection by those who learn they will need medical services in late December and January”);

increased verification of off-season enrollees’ claims to merit a Special Enrollment Period, requiring verification for 100% rather than 50% of applicants (to deter people from finding their way into the marketplace only when they needed care);

a much-increased range of allowable “de minimis” variation from the statutory target for actuarial value at silver, gold and platinum metal levels (allowing plans to vary four points below and two points above the nominal AV, for example from 66% to 72% for silver plans without CSR), and -4/+5 points for bronze; and

increased latitude for states to loosen network adequacy requirements.

A year later, in April 2018, the administration’s final Notice of Benefit and Payment Parameters for the 2019 marketplace (NBPP) did not hold back administrators’ feelings about the program they were bound to administer:

The final rule will mitigate the harmful impacts of Obamacare and empower states to regulate their insurance market. The rule will do this by advancing the Administration’s goals to increase state flexibility, improve affordability, strengthen program integrity, empower consumers, promote stability, and reduce unnecessary regulatory burdens imposed by the Patient Protection and Affordable Care Act.

The 2019 NBPP granted states more “flexibility” in selecting their EHB benchmark plan (the plan that defines in detail the scope of EHBs in that state) by allowing regulators in each state to select a benchmark plan from any other state, i.e., to race to the bottom if they so chose. The rule also eliminated already-weak “meaningful difference” standards that purported to prevent insurers from offering multiple plans with only minor (and often near-invisible) differences.

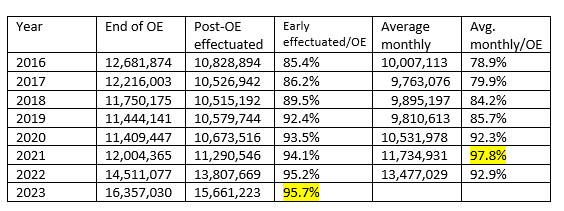

ACA state marketplaces did stabilize from 2018 forward before expanding in the pandemic (especially once propelled by the subsidy boosts enacted in the American Rescue Plan Act). Average premiums, after spiking 21% in 2017 (a year of correction) and 26% in 2018 (a year of political tumult), changed within a range of +1.3% to -3.0% in the years 2019-2022. Off-exchange (unsubsidized) enrollment, while difficult to track, probably stopped shrinking by 2019, after being cut in half by the premium spikes of 2017-18. While on-exchange plan selection as of the end of each Open Enrollment Period dropped in each plan year from 2017 through 2019, average monthly enrollment barely budged — and in fact reached a new high in 2020, fueled by pandemic-driven off-season enrollment.

Sources: CMS Public Use Files and Effectuated Enrollment Snapshots; this post

Whether or not Trump-era regulatory changes helped stabilize premiums and markets, some at least degraded product offerings. Networks grew ever narrower — a change driven mainly by competition and the success of insurers known chiefly for their managed Medicaid plans, but perhaps encouraged by loosened network adequacy standards. In the absence of a “meaningful difference” standard, markets became plagued by a plethora of meaningless choice, to the point where the average ACA shopper had to sort through 114 plans in 2023 (in Miami-Dade County in Florida, the nation’s highest-enrollment county, 224 plans were available). The Trump administration also increased regulatory burdens for prospective enrollees, increasing the chances of being disenrolled or deprived of subsidy for failing to meet various verification requirements.

I asked David Anderson, a former UPMC analyst now finishing a Ph.D. at Duke, about the effects of these insurer-friendly regulations. As to motive, Anderson suggested that HHS and CMS leadership were primarily interested in helping “modestly affluent and healthy families” — those with income somewhat above the 400% FPL cap on subsidy eligibility, the constituency slammed by the sharp rate hikes of 2017 and 2018. He suspects that Tom Price and Seema Verma did not understand (or care about?) the dynamic by which reducing unsubsidized premiums tends to make coverage less affordable for subsidized enrollees (the majority) by reducing premium spreads, and so making plans that cost less than the benchmark more expensive, net of subsidy. In the Trump years, CMS would take measures that might “lose two or three covered unsubsidized lives [enrollments'] to get one unsubsidized life.”

As to the effects on enrollment of these regulatory tweaks, in 2018, Anderson suggested, “silver loading swamped it all.” That is, Trump’s cutoff of CSR reimbursement, and the resulting pricing of CSR into silver plans in most states (see the previous post), made zero-premium plans available to millions more applicants than previously. Then came the pandemic, stimulating an unprecedented surge of off-season enrollments in 2020 (helped by streamlined SEP procedures and, in the state-based marketplaces, emergency SEPs for all). In March 2021 the ARPA subsidy boosts made coverage radically more affordable at all income levels, and a subsequent nationwide emergency SEP — in effect an extended extra Open Enrollment Period — stimulated an enrollment surge that has not yet abated.

The Biden administration has rolled back several regulations designed to boost predictability and profitability for insurers — expanding SEP opportunities, eliminating income verification for those whose incomes might be below the eligibility threshold (mainly in states that had not expanded Medicaid), reducing the number of allowable non-standard plans at each metal level, and tightening network adequacy requirements. Increased affordability enabled by the ARPA subsidies, drawing in more healthy enrollees who might have forgone less affordable offerings, has probably overwhelmed any negative effects these measures may have had on insurer profitability. Increased insurer participation and increased broker commissions suggest as much.

To the extent that the Trump administration harmed actual, prospective and potential marketplace enrollees, it was by nibbling around the regulatory edges. Some of the administration’s insurer-friendly moves may have helped stabilize markets at the margins. Ironically, given Trump’s stated intent, the CSR cutoff gave the markets their biggest boost until the pandemic, the ARPA subsidy boosts, and the Biden administration’s regulatory initiatives made coverage significantly more affordable and somewhat easier to obtain — bringing the Affordable Care Act within credible range of living up to its name.

Photo by cottonbro studio

No comments:

Post a Comment