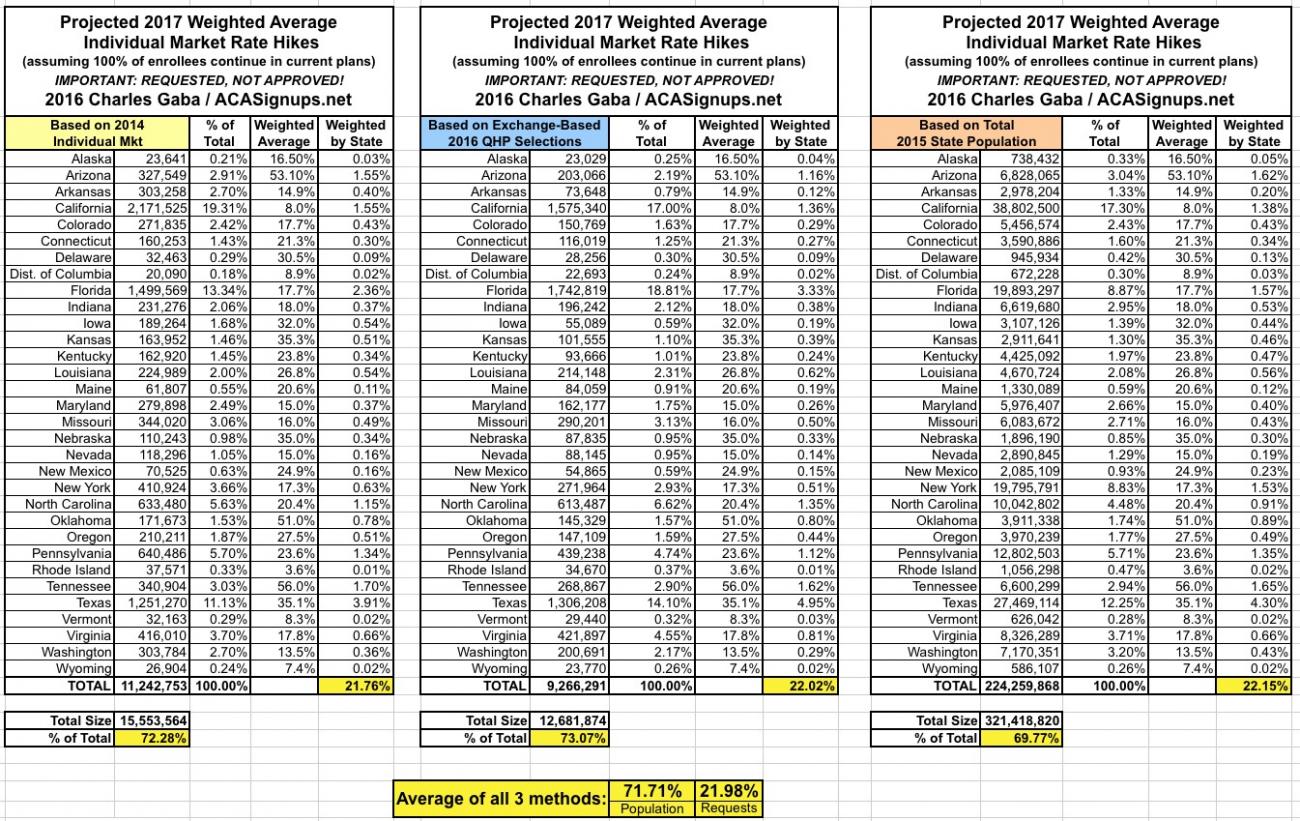

According to Charles Gaba's tracking of health insurers' rate requests for 2017 in the individual market, health insurers have thus far requested a weighted average rate increase of 22%. That's based on reporting from insurers serving 73% of current enrollees.

Rates requested are different from rates approved, however. And approved rates, weighted according to insurers' market share in the previous year, are different from the average rates that people (and the federal government, via subsidies) actually pay. That's because enrollees gravitate toward the cheapest plans at each metal level, which pay the same percentage of costs as more expensive plans in the same metal level.

According to Gaba and HHS, here's how rates shook out in 2015, 2016 and thus far for 2017:

2015

Weighted average requested increase: 8.7%

Weighted average approved increase: 6.9%

Increase in average premium paid on HealthCare.gov: 5.6%

2016

Weighted average requested increase: 13.0%

Weighted average approved increase: 11.6%

Increase in average premium paid on HealthCare.gov: 8.4%

2017

Weighted average requested increase: 22%

Weighted average approved increase: unknown

Avg increase in premium paid on HealthCare.gov: unknown

The requested and approved rate figures are Gaba's; the average premium paid by enrollees on HealthCare.gov (about 3/4 of total marketplace enrollment) is supplied by HHS. Hereafter, following Gaba, we'll call that average increase in paid premiums the effective increase.

Note that the ratio between requested increases and effective increases was nearly identical in 2015 and 2016 -- 64.3% one year, 64.6% the next. If that ratio holds, and if the average weighted request doesn't spike higher by the time all states report, we might expect the average paid premium to increase by 14% this year.

Alternate oracle: benchmark silver

There's another set of tea leaves to read, and that's increases in the price of the benchmark silver plan in each rating area. That's the second-cheapest silver plan, and the cheapest plan is usually (though not always) only a few dollars cheaper. Premium subsidies are set to the benchmark plan, and most people who qualify for premium subsidies also qualify for Cost Sharing Reduction subsidies, which are available only with silver plans. The benchmark can serve is a proxy for cheap silver, and cheap silver is what at least a plurality of marketplace customers buy.

In an April report on 2016 marketplace premiums, HHS noted that the average increase in the second-cheapest silver plan (averaged by state, without weighting), 7.2%, was pretty close to the effective average premium increase, 8% (actually 8.4%, rising from $356 in 2015 to $386 in 2016).

The Kaiser Family Foundation recently published average requested increases in the 2017 benchmark plans in major cities in 13 states plus Washington D.C. The unweighted* average in those 14 cities was 9%. That doesn't tell us much in itself, since the nationwide average requested increase in the benchmark could be much different. Laying those averages beside Gaba's reported weighted requested increases for those 13+1 states, however, as I've done below, yields a ratio that may be worth thinking about. Gaba's weighted state averages are in the far right column; the rest of the data is Kaiser's.

In these fourteen cities, the unweighted* average rate request for second-cheapest silver is up 9% from last year, compared to a 16.3% average requested rate increase for all plans in a state. If we apply that ratio to Gaba's overall weighted average of 22%, it suggests an average requested benchmark increase of 12%. If approved rates are 85% of that (halfway between the requested/approved ratios in 2015 and 2016, according to Gaba), we're at 10.3%. And if, as on HealthCare.gov this year, the effective average price hike for all plans sold is 16.7% higher than the average benchmark increase, that suggests an overall effective average increase of 12%.

That's a lot of "ifs," for sure -- especially since a) the average benchmark increase cited by HHS for 2016 isn't weighted, while Gaba's average requested increases are, both within each state and among states; b) Kaiser's benchmark plan figures are for cities, not states; and c) Gaba suspects that when all requests are reported, the overall weighted average requested increase may climb still higher, perhaps to 25%.

Nonetheless, what is perhaps modestly useful , and worth keeping an eye on over time, is the slower price growth rate for benchmark silver than for the market as a whole. Avalere Health, which recently tracked requested increases in benchmark silver for a smaller sampling of states than Kaiser (9 markets), explains slower price growth at the low end of the silver market as follows:

Finally, it seems fair to expect that the effective average increase for the marketplace in 2017 will be in the 12-15% range (or 12-16%, if the final weighted average for requested increases climbs to 25%). Soon enough we'll know the weighted average approved increase -- and soon enough after that, the effective average hike.

---

* Kaiser gives a weighted average increase for benchmark silver in these markets of 10%. I've left that weighted average off the chart for two reasons: 1) the weighted average is for the cities, not the states in which they're located, and 2) since what matters here is the ratio between requested increases for benchmark silver and requested increases for all plans in a state, I think the weighting of each state is irrelevant

{kind=link}

Rates requested are different from rates approved, however. And approved rates, weighted according to insurers' market share in the previous year, are different from the average rates that people (and the federal government, via subsidies) actually pay. That's because enrollees gravitate toward the cheapest plans at each metal level, which pay the same percentage of costs as more expensive plans in the same metal level.

According to Gaba and HHS, here's how rates shook out in 2015, 2016 and thus far for 2017:

2015

Weighted average requested increase: 8.7%

Weighted average approved increase: 6.9%

Increase in average premium paid on HealthCare.gov: 5.6%

2016

Weighted average requested increase: 13.0%

Weighted average approved increase: 11.6%

Increase in average premium paid on HealthCare.gov: 8.4%

2017

Weighted average requested increase: 22%

Weighted average approved increase: unknown

Avg increase in premium paid on HealthCare.gov: unknown

The requested and approved rate figures are Gaba's; the average premium paid by enrollees on HealthCare.gov (about 3/4 of total marketplace enrollment) is supplied by HHS. Hereafter, following Gaba, we'll call that average increase in paid premiums the effective increase.

Note that the ratio between requested increases and effective increases was nearly identical in 2015 and 2016 -- 64.3% one year, 64.6% the next. If that ratio holds, and if the average weighted request doesn't spike higher by the time all states report, we might expect the average paid premium to increase by 14% this year.

Alternate oracle: benchmark silver

There's another set of tea leaves to read, and that's increases in the price of the benchmark silver plan in each rating area. That's the second-cheapest silver plan, and the cheapest plan is usually (though not always) only a few dollars cheaper. Premium subsidies are set to the benchmark plan, and most people who qualify for premium subsidies also qualify for Cost Sharing Reduction subsidies, which are available only with silver plans. The benchmark can serve is a proxy for cheap silver, and cheap silver is what at least a plurality of marketplace customers buy.

In an April report on 2016 marketplace premiums, HHS noted that the average increase in the second-cheapest silver plan (averaged by state, without weighting), 7.2%, was pretty close to the effective average premium increase, 8% (actually 8.4%, rising from $356 in 2015 to $386 in 2016).

The Kaiser Family Foundation recently published average requested increases in the 2017 benchmark plans in major cities in 13 states plus Washington D.C. The unweighted* average in those 14 cities was 9%. That doesn't tell us much in itself, since the nationwide average requested increase in the benchmark could be much different. Laying those averages beside Gaba's reported weighted requested increases for those 13+1 states, however, as I've done below, yields a ratio that may be worth thinking about. Gaba's weighted state averages are in the far right column; the rest of the data is Kaiser's.

In these fourteen cities, the unweighted* average rate request for second-cheapest silver is up 9% from last year, compared to a 16.3% average requested rate increase for all plans in a state. If we apply that ratio to Gaba's overall weighted average of 22%, it suggests an average requested benchmark increase of 12%. If approved rates are 85% of that (halfway between the requested/approved ratios in 2015 and 2016, according to Gaba), we're at 10.3%. And if, as on HealthCare.gov this year, the effective average price hike for all plans sold is 16.7% higher than the average benchmark increase, that suggests an overall effective average increase of 12%.

That's a lot of "ifs," for sure -- especially since a) the average benchmark increase cited by HHS for 2016 isn't weighted, while Gaba's average requested increases are, both within each state and among states; b) Kaiser's benchmark plan figures are for cities, not states; and c) Gaba suspects that when all requests are reported, the overall weighted average requested increase may climb still higher, perhaps to 25%.

Nonetheless, what is perhaps modestly useful , and worth keeping an eye on over time, is the slower price growth rate for benchmark silver than for the market as a whole. Avalere Health, which recently tracked requested increases in benchmark silver for a smaller sampling of states than Kaiser (9 markets), explains slower price growth at the low end of the silver market as follows:

Lower-cost silver plans tend to be most popular with consumers, making this portion of the market more competitive as plans seek to attract enrollees.Further it may prove true over time that the effective average price increase for the whole market -- again, the average of all premiums paid in a given year -- is closer to the average benchmark plan increase than to the average weighted increase for all plans sold in the previous year.

Finally, it seems fair to expect that the effective average increase for the marketplace in 2017 will be in the 12-15% range (or 12-16%, if the final weighted average for requested increases climbs to 25%). Soon enough we'll know the weighted average approved increase -- and soon enough after that, the effective average hike.

---

* Kaiser gives a weighted average increase for benchmark silver in these markets of 10%. I've left that weighted average off the chart for two reasons: 1) the weighted average is for the cities, not the states in which they're located, and 2) since what matters here is the ratio between requested increases for benchmark silver and requested increases for all plans in a state, I think the weighting of each state is irrelevant

No comments:

Post a Comment