Note: Free xpostfactoid subscription is available on Substack alone, though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up.

|

| This year's NJ marketplace has feet of bronze |

GetCoveredNJ, New Jersey’s state ACA marketplace, has released its final enrollment snapshot for OEP 2026. Enrollment is down less than 1% from OEP 2025, but attrition when people have to make their first premium payments — and, if they get that far, sustain higher payments year-long — will probably drop average monthly enrollment well below the 2025 level. * In particular, the 211,289 renewing enrollees who passively auto-re-enrolled may react to sticker shock. (Conversely, a very sharp spike in active re-enrollments, from 85,177 in 2025 to 219,933 in 2026, points to a large potential well of resilience — people who noted the premium spikes and made a conscious choice.)

As the enrollment report emphasizes, premiums rose sharply for most enrollees in 2026, whether or not they lost subsidy eligibility. In 2025, 44% of all enrollees had paid less than $10/month in premiums; this year, just 10% will. Last year, 28% of enrollees paid more than $100/month; this year, 44% have crossed that threshold. This year, 18% of enrollees obtained no federal subsidy ; last year, just 9% went without APTC. (A third of those who are ineligible for federal subsidies obtained smaller state supplemental subsidies, available at incomes up to 600% FPL.) See Gaba for a finer-grained breakdown of net-of-subsidy premiums paid.

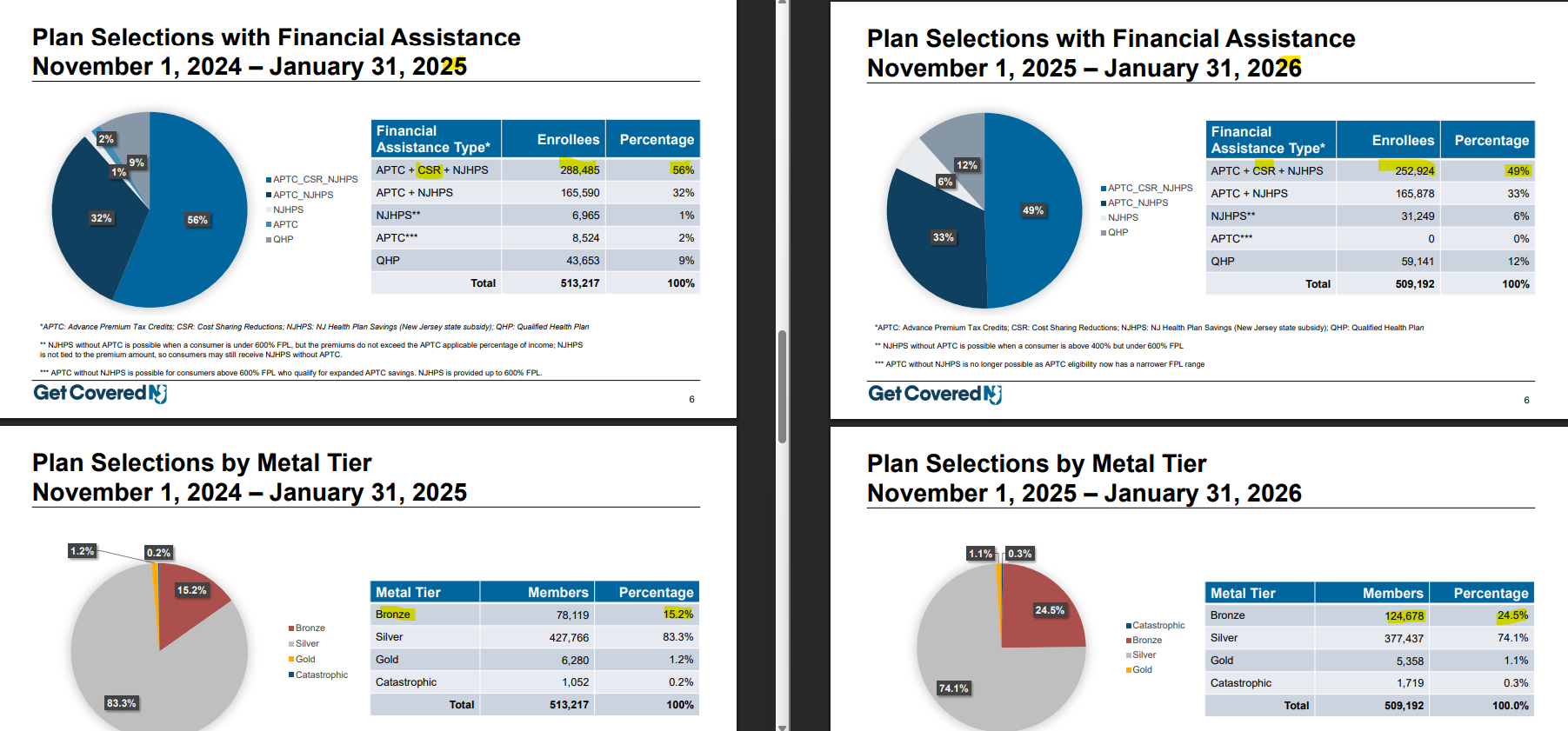

I want to focus here on coverage degradation in 2026 — a down-shifting in metal level. In New Jersey, that means almost entirely a switch from silver plans to bronze, because in NJ, gold plans are effectively unaffordable, chosen by just 1% of enrollees in 2025 and 2026 alike. The Jersey marketplace has always been dominated by silver plans, but in 2026 silver selection dropped to 74.1%, down from 83.3% in 2025.

To take the full measure of a shift from silver to bronze, we need to know about silver selection at incomes where Cost Sharing Reduction (CSR) attaches to silver plans. CSR raises the actuarial value of a silver plan from a baseline of 70% (vs. 60% for bronze) to 94% at incomes up to 150%o of the federal poverty level (FPL), to 87% at incomes in the 150-200% FPL range, and to 73% for those in the 200-250% FPL income bracket. At incomes over 250% FPL, no CSR is available.

As shown below, CSR enrollment dropped by 12% in 2026, from 288,485 to 252,924, a drop of 35,561, about 80% of whom were likely eligible for 94% or 87% AV silver. The percentage of all enrollees obtaining CSR dropped from 56% in 2025 to 49% in 2026.

To get a full sense of lost actuarial value/increased out-of-pocket exposure, we would need to know how many people dropped from silver to bronze in each income bracket — as we will in March or April, if CMS follows past schedules in publishing the Public Use Files for marketplace enrollment. But we can get a pretty good idea now. The drop in silver selection was proportionate among those eligible and ineligible for CSR (i.e., those with incomes below/above 250% FPL). In both 2025 and 2026, 33% of silver plan enrollees did not obtain CSR.

Given that proportionality, I think it pretty likely that the distribution of silver plan selection across each income bracket in 2026 will be pretty similar to the 2025 distribution. In 2025, 30% of silver plan enrollees had income below 150% FPL; 27% had income in the 150-200% FPL range; 13% had income in the 200-250% FPL range, and 30% had income above 250% FPL.** That comes out to an average silver plan actuarial value of 82%.

Using that 82% average AV for silver enrollees, by my calculations the average AV obtained by all enrollees at all metal levels in the New Jersey marketplace was 79.5% in 2025 and 78.1% in 2026.

That’s not a huge difference. On some level, I am impressed by the resilience of low-income enrollees who stuck with silver — though it remains to be seen how many stay in the marketplace. For a single 40 year-old in Essex County with an annual income of $23,000 —just under 150% FPL — the lowest-cost silver plan would have been free in 2025 but costs $50/month in 2026. That’s a lot, at that income. Bronze plans are still available for zero premium. At an income of $31,000, just under 200% FPL, lowest-cost silver is $128/month this year, vs. $34/month for lowest-cost bronze. Last year, the benchmark (second cheapest) silver plan would have been $52/month.

The effects of the expiration in 2026 of the enhanced subsidies enacted in the American Rescue Plan Act in March 2021 will take a while to unfold - and still longer to show up statistically, as average monthly enrollment for 2026 probably won’t be published until mid-2027. The relatively small initial drop in enrollment may embolden Republicans to continue to accede to Trump’s wish not to extend them. In that case, we’ll see what the marketplace looks like in 2028— if Republicans don’t take further measures to degrade or more or less wholly eliminate it.

— — —

*The year-over-year drop in average monthly enrollment may be particularly sharp in New Jersey, since the Trump administration cut off year-round enrollment at low incomes in August 2025, and the Republican megabill enacted last July effectively codified the prohibition. New Jersey allowed year-round enrollment for enrollees with income up to 200% FPL, in contrast to the 150% FPL ceiling in other states, initiated by the Biden administration in 2022. Furthermore, new selections are down 31%, from 112,699 in 2025 to 77,970 in 2026.

**Let me note a couple of uncertainties regarding silver plan AV: 1) the 30% with income below 150% FPL in NJ in 2025 includes 5% with income below 100% FPL, some of whom probably were not subsidy-eligible and so did not obtain CSR (occasional windows into enrollment under 100% FPL indicate as much). For AV purposes, I subtracted a percentage point from the population under 150% FPL and added that point to those obtaining silver with no CSR. 2) The GetCoveredNJ 2025 report shows 33% of silver enrollees with no CSR, whereas the income breakout in the PUF, which uses rounded percentages, shows 30% of silver enrollees over 250% FPL (or not reporting income). At every income level, a small percentage of enrollees obtain no subsidy, and so no CSR.

No comments:

Post a Comment