|

| Garden State, from certain angles |

New Jersey is one of 8 states* that supplement federal premium subsidies in the ACA marketplace with state-funded "wraparound" subsidies that further reduce enrollees' costs. New Jersey's supplementary subsidies are funded by a state tax on health insurers implemented in July 2020 after Congress repealed a similar tax assessed nationally.

New Jersey's state subsidies rise with income. That works well in the era of the enhanced federal subsidies created by the American Rescue Plan ACA in March 2020 and extended through 2025 by the Inflation Reduction Act, enacted this past summer. ARPA rendered benchmark silver coverage free at incomes up to 150% FPL and rising to just 2% of income at 200% FPL (for a single person, about $45/month at an income of $27,180). New Jersey's wraparound subsidies all but zero out premiums for benchmark silver up to 200% FPL, as they add $40 per month for an individual and twice that for a family with income in the 150-200% FPL range. (You can explore plans and prices at different incomes and ages with the plan preview tool at GetCoveredNJ, the state exchange.)

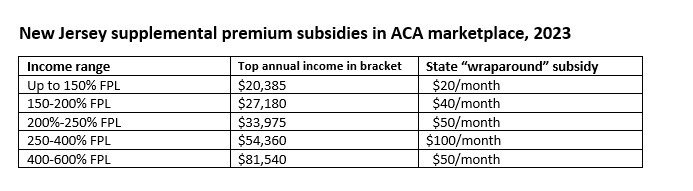

The break points between the state subsidy levels do create some odd effects, however. They run as follows for an individual, with twice as much allocated for a family of two or more.

There are two rather sharp breaks here. One is at just over 250% FPL ($45,775/yr for a couple). For a couple with an annual income just under that threshold (say, $45,000), the state subsidy is $100/month; bump that income up to $46,000, and the state subsidy rises to $200/month. The reverse happens at 400% FPL: a subsidy of $200/month for a couple with an income of $73,000, dropping to $100/month on the far side of $73,240.

Up to 400% FPL, this subsidy structure compensates higher incomes not only by partly offsetting the federal subsidies’ sliding scale (in which the percentage of income required for a benchmark silver plan rises with income), but by effectively compensating enrollees for each step-down in the federal Cost Sharing Reduction (CSR) subsidies that attach to silver plans at incomes up to 250% FPL. CSR raises the actuarial value of a silver plan from a baseline of 70% with no CSR to 94% at incomes up to 150% FPL, 87% in the 150-200% FPL bracket, and a weak 73% at 200-250% FPL.

The state subsidy increase at 250% FPL creates the oddest effects, both because it’s the largest increase ($100/month for a family) and because CSR just below 250% FPL is almost hard to notice. When income passes the 250% FPL threshold, premiums (net of subsidy) go down, rather sharply. It doesn't matter much for those who choose the benchmark (second cheapest) or cheapest silver plan -- premiums for those plans are low at incomes near 250% FPL, massively subsidized as they are by the ARPA-enhanced federal subsidies and the state supplemental. At an income of $45,000, just under 250% FPL for a couple of 40 year-olds, the cheapest silver plan costs just $29/month for the two of them, and the benchmark, $43/month.

But this year Aetna entered the New Jersey market and grabbed the lowest price points with a narrow network that leaves out major hospitals. The cheapest silver plan from AmeriHealth, which had dominated the New Jersey marketplace's lowest price points until 2023 and offers a network that includes most of the state's major hospitals, will cost this couple $72 per month. Bump the income estimate up from $45,000 to $46,000, and -- hey presto! -- the two cheapest AmeriHealth plans are available for zero premium.

While CSR reduces out-of-pocket costs dramatically at incomes up to 200% FPL, it's a pale shadow at 200-250% FPL, offering only a marginal improvement over a silver plan without CSR. The chief advantage offered by CSR at this level is reduction in the highest allowable annual out-of-pocket maximum -- capped by law at $7,250 for a single person with this level of CSR, compared to $9,100 for a plan without CSR. Those limits are double for a family (including a couple). In 2023, the cheapest AmeriHealth silver plan in most of the state at the weakest CSR level has an out-of-pocket maximum of $13,700, compared to $16,200 with no CSR. Is that worth $72 per month? Only if you have good reason to think your medical costs will approach the OOP max.

I have emphasized recently that knowing the break points at which ACA subsidies and benefits change can be very valuable to applicants, given that the subsidy is based on an estimate of future income, and many if not most family incomes have many variables. Filtering in the New Jersey break points — and recognizing their effects — makes the shopping on GetCoveredNJ almost as mind-bending as picking the most cost-effective option in the toilet paper aisle.

-----

* Two other states, New York and Minnesota, offer separate low-cost Basic Health Programs to enrollees with income up to 200% FPL. For a summary of state supplemental programs, see Charles Gaba or Louise Norris

Thanks Andrew. A good read as usual.

ReplyDelete