Subscribe (free) to xpostfactoid

|

| Free in 2023 |

Senate Democrats' passage of the Inflation Reduction Act yesterday evening was an exercise in the art of the possible, the culmination of a year-long immersion in the reality principle. Senate Democrats as a body probed to the last minute what first Manchin and finally Sinema would allow them to pass, and ultimately maxed out on that allowance.

The result is powerful legislation that gives us a fighting chance to mitigate the worst effects of climate change and sets up a starter home for Medicare to negotiate prescription drug prices. It also boosts the perhaps still-long odds that Democrats can hold the Senate and House and so stave off the Republican threat to democracy itself.

While the bill's most powerful potential impact (if not undone by Republicans) will likely come from its stimulus to clean energy development and reduction of greenhouse gas emissions, our focus here is healthcare, as always. The bill's Medicare provisions mostly survived, though the Senate parliamentarian ruled that the inflation caps on drug prices (discussed in detail in the prior post) could only apply to Medicare, not to the commercial market, and Senate Republicans blocked an amendment that would have extended a $35/month cap on insulin costs to the commercial as well as Medicare markets. The pare-back of the inflation caps struck out $38 billion in revenue over 10 years forecast by the CBO (anticipated from savings to employer health plans plowed into taxable income) and perhaps half of the $62 billion in forecast savings from the inflation rebates, which would have applied to all drugs sold in the commercial as well as Medicare markets.

Early last week, as debate over the bill commenced, Bernie Sanders, offering only grudging support to a bill that ultimately spends not much more than a tenth of the amount he originally mapped for investments in Democratic priorities, belittled the Medicare provisions, lamenting, ""You're not going to see any changes over the next four years...This bill does nothing to lower prescription drug prices for anyone who is not on Medicare."

The second proposition -- that the inflation caps won't help anyone outside of Medicare -- is debatable and contrary to CBO analysis. The first assertion -- that no changes will occur until 2026, when Medicare's price negotiations for targeted drugs begin -- is flat-out wrong.

As I noted in the prior post, the inflation caps (pared back though they now are) begin in 2023, along with the elimination of copays in Medicare Part D for vaccines. A more sweeping reduction of enrollees' cost exposure, the $2,000 cap on Part D out-of-pocket (OOP) costs, begins in 2025.

Moreover, a de facto OOP cap of about $3,000 begins in 2024, when Part D enrollees' responsibility for any share of their drug costs after they max out of the current "catastrophic phase" of coverage ends. At present, Part D enrollees whose total spending exceeds the catastrophic cap pay 5% of any further costs, which for a cancer drug costing tens of thousands of dollars per month can be substantial. In 2022, the enrollee's share of costs through the catastrophic phase was $2,937. Allowing for inflation adjustments, that will be the maximum OOP exposure for Part D enrollees in 2024 -- call it a $3,200 cap.

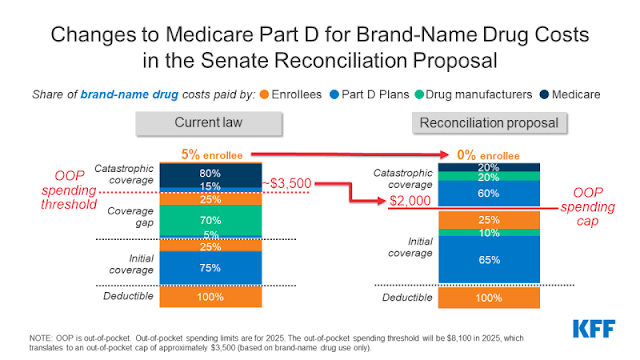

In 2025, the dizzyingly complex formula* for who pays what in Medicare Part D changes radically, and enrollees' OOP cap goes down to $2,000 (other payers include Part D plans, a federal reinsurance program, and drug manufacturers).

Also in 2024, the eligibility threshold for the full low-income support (LIS) benefit in Part D rises from 135% of the Federal Poverty Level to 150% FPL. At present, those with income in the 135-150% FPL range get only a partial low-income benefit. This bump-up is important, because the majority of enrollees with high out-of-pocket costs do qualify for LIS, and the full benefit limits out-of-pocket costs to single digits per prescription and to zero if an enrollee's total drug costs (paid by all payers) reach Part D's catastrophic phase (currently $4,430).

According to the Kaiser Family Foundation (KFF), in 2020, 1.4 million Part D enrollees spent more than $2,000 out of pocket. In 2019, also per KFF, about 300,000 spent more than $3,100. Most enrollees whose total spending hits the catastrophic cap, however, are eligible for LIS; in 2017, according to another KFF report, of 3.6 million enrollees whose total spending (by all payers) hit the catastrophic cap, 2.6 million were LIS beneficiaries. In 2020, per KFF, 400,000 Part D enrollees were on partial low income support; their successors in 2024 will likely benefit from extension of the full LIS benefit.

In sum, then, in 2024 several hundred thousand Part D enrollees should find their OOP costs reduced, and in 2025 the number of beneficiaries helped by the OOP reductions will rise to about 2 million. While each year, only about 2-3% of enrollees spend more $2,000 out of pocket**, a higher percentage will reach that level of all-payer spending (currently $7,050) at some point in their Medicare years, and so benefit from the OOP cap.

Update: Yet another KFF analysis found that over five years, about twice as many Part D enrollees had at least one year in which their OOP spending exceeded the catastrophic cap (again, about $3,000 at present) as in any given year (2.7 million from 2015-2019). Since any of us, in any given year, could contract an illness that would put us over a $2,000 cap, the measure provides important security for all current and future Medicare enrollees who don't qualify for LIS -- that is, ultimately, most Americans.

Finally, the Inflation Reduction Act eliminates co-pays for vaccines for Part D enrollees in 2023 (including the Shingrix vaccine, which normally costs about $190, paid in full by enrollees who haven't met their Part D deductible). In 2020, per KFF, 4.1 million Part D enrollees received a covered vaccine.

----

* Courtesy of KFF, here is how the formula will change in 2025:

No comments:

Post a Comment