Paul Krugman crows a bit about the ACA's relative resilience:

But Krugman overstates the case on several fronts -- the most notorious being a straight factual fudge. Noting that 83% of enrollees on the exchanges are subsidized, he concludes:

And their ranks are shrinking. The Brookings Institute's Matt Fiedler estimated last fall that premium hikes averaging 20.5% in 2017 were likely to reduce unsubsidized enrollment by 12.3%. Premium increases were even steeper in 2018 and are likely to be very high again in 2019. An Urban Institute report** estimates that if Trump's proposed rules promoting sale of short-term plans take full effect, 6.5 million more people will be uninsured in 2019 than would have been had Republican sabotage efforts in the Trump era (CSR funding cutoff, slashing of outreach/advertisement, promotion of short-term and association health plans) not occurred.

As for the alleged brilliance of building a system resilient to shocks: the ACA marketplace could have been made a lot more resilient, on multiple fronts. First, the bill's authors could have made the three risk management programs for insurers (reinsurance, risk corridors and risk adjustment) permanent and unambiguously funded -- as they are in Medicare Part D (from which they were modeled), created by -- surprise! -- Republicans. In the ACA, two of these programs phased out after three years, and funding for one -- the risk corridors -- was gutted by the Republican Congress, precipitating the collapse of most of the nonprofit health insurance coops founded under the ACA (and underfunded, in other destabilizing swipes).

More fundamentally, ACA subsidies were underfunded. This was obvious as soon as Obama imposed a $900 billion price cap on the whole program, and when the Senate Finance Committee bill was first introduced (though the subsidies in that bill were enriched somewhat in the final). Richard Kirsch, a key activist in the fight to pass the ACA, spotlighted the inadequacy of the subsidies in his 2011 book about the struggle, as I recounted in some detail here. The subsidies are particularly skimpy in the 200-400% FPL range. For a youngish, healthy solo person with an income of $30,000, a silver plan costing $200 per month with a $3,000 deductible does not look too attractive.

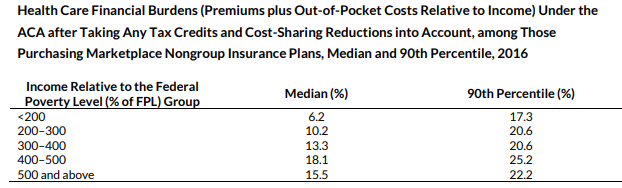

Finally, as noted above, steep premium hikes have rendered coverage unaffordable for many with incomes over the subsidy threshold of 400% FPL. In fact, those premiums were affordable only by the most tenuous definition for many in the 400-500% FPL range (and above) from the start. In 2015, the Urban Institute's Linda Blumberg and John Holahan found that enrollees in that income range were paying a higher percentage of income for insurance and healthcare than any other income group (and that costs were too high at every income level):

Recognizing at that fairly early point (August 2015) that ACA marketplace subsidies were not adequate to the task, Blumberg and Holahan proposed an enriched subsidy schedule that reduced premiums and out-of-pocket costs at every income level -- and capped premiums at 8.5% of income for all comers. That proposal is now the basis of "ACA 2.0" bills introduced this year in the Senate and House, as discussed here.

Finally, the ACA marketplace would be more popular, more sustainable and more affordable if it had been structured like other government-funded insurance programs that work through private insurers: Medicare Advantage and managed Medicaid. Both programs effectively cap the rates that insurers pay providers. MA plans' provider rates are effectively tethered to those the government pays for traditional Medicare, and managed Medicaid contracts, which vary by state, keep insurers paying rates comparable to fee-for-service Medicaid. Creating a marketplace in which insurers freely negotiated their own payment rates as in the employer market was a design that reduced resilience.

To ease up on the ACA's creators a bit, the kind of reforms and subsidy-sweetening proposed by Blumberg and Holahan would represent a fairly normal adjustment to a new benefit program. The ultimate ACA sabotage is to block any improvement. Ironically, the estimated cost of the Blumberg-Holahan package ($220 billion over ten years, as of 2015) is pretty close to the cost of a measure undertaken out of pure spite -- Trump's cutoff of CSR reimbursement to insurers, which inefficiently boosts subsidies and was estimated by CBO to cost $194 billion over ten years (an estimate now reduced by Republicans' repeal of the individual mandate, which will reduce enrollment).

Income-based subsidies did endow the marketplace with a measure of resilience, as Krugman suggests. And the ACA Medicaid expansion, much less frequently discussed, is a major success, though Republicans have aimed both mortal and merely disfiguring blows against it, too. But touting ACA design as "brilliant" overstates the case.

P.S. As a reader pointed out to me, Krugman's main point is that the fate of not just the ACA but any drive toward universal coverage hinges on Democrats taking at least one house of Congress:

--

* Today Charles Gaba pegs the total number of unsubsidized enrollees in ACA-compliant plans at 6.8 million, 4.9 million of them off-exchange (scroll down; it's a long, multi-topic post).

**By Linda Blumberg Matthew Buettgens and Robin Wang.

What’s the secret of Obamacare’s stability? The answer, although nobody will believe it, is that the people who designed the program were extremely smart. Political reality forced them to build a Rube Goldberg device, a complex scheme to achieve basically simple goals; every progressive health expert I know would have been happy to extend Medicare to everyone, but that just wasn’t going to happen. But they did manage to create a system that’s pretty robust to shocks, including the shock of a White House that wants to destroy it.Um, maybe, sort of. The perspective is a useful corrective to those of us prone to lamenting the ACA's many design flaws and susceptibility to sabotage. And Krugman does highlight a resilience-making feature that I suppose could have been otherwise:

Those subsidies aren’t fixed. Instead, the formula sets the subsidy high enough to put a limit on how high premium payments can go as a percentage of income.Yes, the subsidy-eligible are insulated from the massive premium hikes of the past two years -- averaging well over 20% in each year -- and that would not be the case if they were not benchmarked to income. The Trump administration even added some accidental extra resilience in an act of spite -- cutting off federal CSR reimbursements to insurers -- which simply boosted the subsidies, and allowed many enrollees to leverage the increase by buying bronze or gold plan (since in most states insurers concentrated the un-reimbursed price of CSR in silver plans, against which subsidies are set). So the subsidy structure seems to preserve a pool of 8 million subsidized -- if erosion among the unsubsidized, and the Trump administration's fostering of a lightly regulated, medically underwritten alternative market for the healthy among them -- doesn't drive large numbers of insurers out.

But Krugman overstates the case on several fronts -- the most notorious being a straight factual fudge. Noting that 83% of enrollees on the exchanges are subsidized, he concludes:

of the 27 million Americans who have either gained coverage through the Medicaid expansion or purchased insurance on the exchanges, only about two million are exposed to those Trump-engineered premium hikes. That’s still a lot of people, but it’s not enough to get a death spiral going.Left out of this equation are 4-5 million enrollees in ACA-compliant plans bought off-exchange.* Like unsubsidized on-exchange enrollees, they are bearing the full brunt of enormous premium hikes -- with more expected, thanks to the next wave of Republican sabotage (repeal of the individual mandate penalty, and promotion of short-term and association health plans). Unsubsidized enrollees represent about 40% of the ACA-compliant market.

And their ranks are shrinking. The Brookings Institute's Matt Fiedler estimated last fall that premium hikes averaging 20.5% in 2017 were likely to reduce unsubsidized enrollment by 12.3%. Premium increases were even steeper in 2018 and are likely to be very high again in 2019. An Urban Institute report** estimates that if Trump's proposed rules promoting sale of short-term plans take full effect, 6.5 million more people will be uninsured in 2019 than would have been had Republican sabotage efforts in the Trump era (CSR funding cutoff, slashing of outreach/advertisement, promotion of short-term and association health plans) not occurred.

As for the alleged brilliance of building a system resilient to shocks: the ACA marketplace could have been made a lot more resilient, on multiple fronts. First, the bill's authors could have made the three risk management programs for insurers (reinsurance, risk corridors and risk adjustment) permanent and unambiguously funded -- as they are in Medicare Part D (from which they were modeled), created by -- surprise! -- Republicans. In the ACA, two of these programs phased out after three years, and funding for one -- the risk corridors -- was gutted by the Republican Congress, precipitating the collapse of most of the nonprofit health insurance coops founded under the ACA (and underfunded, in other destabilizing swipes).

More fundamentally, ACA subsidies were underfunded. This was obvious as soon as Obama imposed a $900 billion price cap on the whole program, and when the Senate Finance Committee bill was first introduced (though the subsidies in that bill were enriched somewhat in the final). Richard Kirsch, a key activist in the fight to pass the ACA, spotlighted the inadequacy of the subsidies in his 2011 book about the struggle, as I recounted in some detail here. The subsidies are particularly skimpy in the 200-400% FPL range. For a youngish, healthy solo person with an income of $30,000, a silver plan costing $200 per month with a $3,000 deductible does not look too attractive.

Finally, as noted above, steep premium hikes have rendered coverage unaffordable for many with incomes over the subsidy threshold of 400% FPL. In fact, those premiums were affordable only by the most tenuous definition for many in the 400-500% FPL range (and above) from the start. In 2015, the Urban Institute's Linda Blumberg and John Holahan found that enrollees in that income range were paying a higher percentage of income for insurance and healthcare than any other income group (and that costs were too high at every income level):

Recognizing at that fairly early point (August 2015) that ACA marketplace subsidies were not adequate to the task, Blumberg and Holahan proposed an enriched subsidy schedule that reduced premiums and out-of-pocket costs at every income level -- and capped premiums at 8.5% of income for all comers. That proposal is now the basis of "ACA 2.0" bills introduced this year in the Senate and House, as discussed here.

Finally, the ACA marketplace would be more popular, more sustainable and more affordable if it had been structured like other government-funded insurance programs that work through private insurers: Medicare Advantage and managed Medicaid. Both programs effectively cap the rates that insurers pay providers. MA plans' provider rates are effectively tethered to those the government pays for traditional Medicare, and managed Medicaid contracts, which vary by state, keep insurers paying rates comparable to fee-for-service Medicaid. Creating a marketplace in which insurers freely negotiated their own payment rates as in the employer market was a design that reduced resilience.

To ease up on the ACA's creators a bit, the kind of reforms and subsidy-sweetening proposed by Blumberg and Holahan would represent a fairly normal adjustment to a new benefit program. The ultimate ACA sabotage is to block any improvement. Ironically, the estimated cost of the Blumberg-Holahan package ($220 billion over ten years, as of 2015) is pretty close to the cost of a measure undertaken out of pure spite -- Trump's cutoff of CSR reimbursement to insurers, which inefficiently boosts subsidies and was estimated by CBO to cost $194 billion over ten years (an estimate now reduced by Republicans' repeal of the individual mandate, which will reduce enrollment).

Income-based subsidies did endow the marketplace with a measure of resilience, as Krugman suggests. And the ACA Medicaid expansion, much less frequently discussed, is a major success, though Republicans have aimed both mortal and merely disfiguring blows against it, too. But touting ACA design as "brilliant" overstates the case.

P.S. As a reader pointed out to me, Krugman's main point is that the fate of not just the ACA but any drive toward universal coverage hinges on Democrats taking at least one house of Congress:

...if Republicans manage to hold on to Congress, they will make another all-out push to destroy the act — because they’ll know that it’s probably their last chance. Indeed, if they don’t kill Obamacare soon, the next step will probably be an enhanced program that lets Americans of all ages buy into Medicare.And on that front, Krugman is dead on, of course.

--

* Today Charles Gaba pegs the total number of unsubsidized enrollees in ACA-compliant plans at 6.8 million, 4.9 million of them off-exchange (scroll down; it's a long, multi-topic post).

**By Linda Blumberg Matthew Buettgens and Robin Wang.

Well done as always.

ReplyDeleteThere are fascinating articles in actuarial journals about the history of Medicare Advantage plans. A few years after the program began, some carriers were bailing out and prices were rising.

So the federal government raised payment rates, on a bipartisan basis.

The Democrats did not refuse participation just because George Bush had sponsored the original program.

Also of course, no one in Washington wants to tick off senior citizens. Whereas there is no political penalty for ticking off working people or the unemployed.

Krugman is wrong to say that the ACA is resilient. If the Republicans had not catered to their Social Darwinist arm (the Freedom Caucus), they could have repealed much of the ACA with just basic party discipline.

That is hardly a definition of resilient.