Certainly not for everyone. And certainly not for the federal government, which foots the bulk of the premium bill for most marketplace enrollees. But for many and perhaps most subsidized buyers, a silver plan will available for less than they paid in 2016 (or would have paid, had they enrolled).

That's my takeaway from an Avalere Health analysis of rate request data in eight states plus Washington D.C., released last week.

You may have read that rate requests from health insurers selling ACA-compliant plans are in the 20% range on average. That's true, as far as it goes. And while rate requests are not the same as rate approvals, there may not be much daylight between them in most states this year.

At the same time, as Avalere points out, the total set of plans that insurers bring to market and the smaller set of plans that most customers actually buy are very different things. In the ACA marketplace, 69% of buyers selected silver plans, which for most buyers come with Cost Sharing Reduction (CSR) subsidies not available with other metal levels. Moreover, as Avalere stresses, most silver plan purchases are concentrated among the cheapest plans available at that metal level. And in that most competitive market segment, Avalere finds, price hikes are more modest than in the market as a whole.

I would take this price impact analysis a step further. Among the roughly 53% of individual market enrollees who are subsidized*, what matters most price-wise is not the absolute price of a plan but the price spread between the plan they want and the benchmark second-cheapest silver plan, which determines their subsidy. If the benchmark plan price goes up, the subsidy goes up proportionately. And the price spread that looms largest is between the cheapest and second-cheapest (benchmark) silver plan. That spread represents a discount on silver coverage -- which means a discount on CSR for the three quarters-plus of subsidized buyers who qualify for CSR.

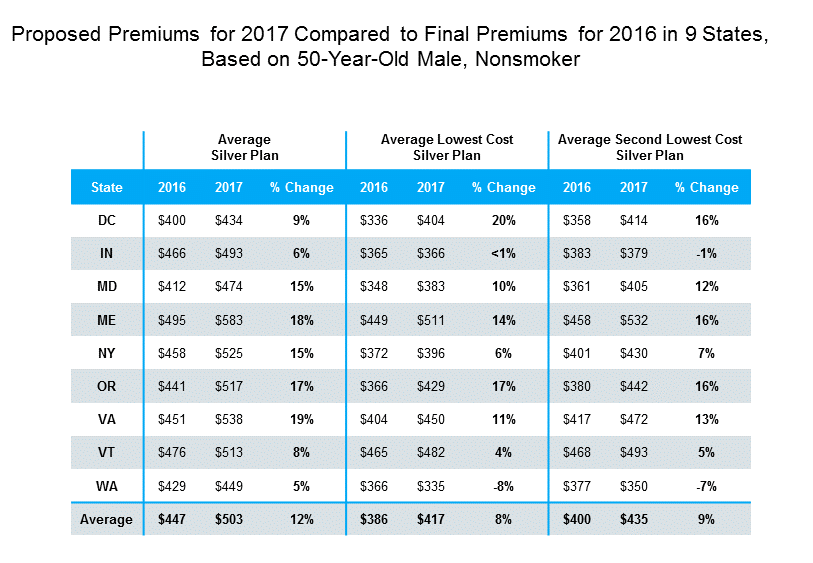

Avalere's analysis of the nine states (including D.C.) for which it had data indicates that benchmark silver plan rate requests are for an average increase of 9% in those states, while for cheapest silver plans the requested increase averages 8%. That compares to an average 12% requested increase for all silver plans in each state, which in turn is probably lower than the average requested for plans at all metal levels. Here's Avalere's breakdown for silver:

Note that in six of the nine markets, the spread between the average cheapest and second cheapest (benchmark) silver has increased [but see update re Kaiser sampling below - 6/15]. Here are the spreads:

Note that in six of the nine markets, the spread between the average cheapest and second cheapest (benchmark) silver has increased [but see update re Kaiser sampling below - 6/15]. Here are the spreads:

Average Prices Between Cheapest and Second-Cheapest Silver

Multiple caveats are in order. First, rates requested do not equal rates approved. Second, the average spread in a given state masks differences in different rating areas within that state. Third, a modest increase in the percentage of income that subsidized buyers will be asked to pay for the benchmark may roughly equal the average increase in "silver discount" indicated here. Fourth this is a sampling of just nine states (including DC). And finally, almost half of individual market enrollees are unsubsidized, and to them, the spread will vary by age. For those with incomes over 250% FPL, subsidized or unsubsidized, the spread will not pack the extra wallop of providing access to CSR at a discount.

Nonetheless, the snapshot is at least suggestive. Intense competition to offer cheapest silver does limit price increases at the bottom of the silver spectrum -- and last year, the average spreads between cheapest and benchmark silver did widen slightly. Perhaps coincidentally, CSR takeup seems to have risen in the 38 states that used HealthCare.gov in 2016.

All politics may not be local any more, but the ACA marketplace definitely is.

UPDATE 6/15: Today the Kaiser Family Foundation released an analysis of requested benchmark silver and cheapest silver prices in the largest urban areas in 14 states that have provided enough information to do such analysis. In eight out of fourteen, the requested rates for cheapest silver went up more than for the benchmark. On average, the cheapest silver request was up 11% and the benchmark, 10% -- the reverse of the Avalere comparison, in which the average requested benchmark increase was a percentage point higher than the average cheapest silver increase. In sum, local variation is tremendous, and the relationship between cheapest silver and benchmark silver pricing is probably pretty random, except in cases in which one insurer grabs both slots, which is not uncommon (and generally spells a negligible spread).

----

* According to the Kaiser Family Foundation's latest nongroup market survey, 64% of all nongroup market enrollees are in marketplace plans. 83% of marketplace enrollees are subsidized.

That's my takeaway from an Avalere Health analysis of rate request data in eight states plus Washington D.C., released last week.

You may have read that rate requests from health insurers selling ACA-compliant plans are in the 20% range on average. That's true, as far as it goes. And while rate requests are not the same as rate approvals, there may not be much daylight between them in most states this year.

At the same time, as Avalere points out, the total set of plans that insurers bring to market and the smaller set of plans that most customers actually buy are very different things. In the ACA marketplace, 69% of buyers selected silver plans, which for most buyers come with Cost Sharing Reduction (CSR) subsidies not available with other metal levels. Moreover, as Avalere stresses, most silver plan purchases are concentrated among the cheapest plans available at that metal level. And in that most competitive market segment, Avalere finds, price hikes are more modest than in the market as a whole.

I would take this price impact analysis a step further. Among the roughly 53% of individual market enrollees who are subsidized*, what matters most price-wise is not the absolute price of a plan but the price spread between the plan they want and the benchmark second-cheapest silver plan, which determines their subsidy. If the benchmark plan price goes up, the subsidy goes up proportionately. And the price spread that looms largest is between the cheapest and second-cheapest (benchmark) silver plan. That spread represents a discount on silver coverage -- which means a discount on CSR for the three quarters-plus of subsidized buyers who qualify for CSR.

Avalere's analysis of the nine states (including D.C.) for which it had data indicates that benchmark silver plan rate requests are for an average increase of 9% in those states, while for cheapest silver plans the requested increase averages 8%. That compares to an average 12% requested increase for all silver plans in each state, which in turn is probably lower than the average requested for plans at all metal levels. Here's Avalere's breakdown for silver:

Average Prices Between Cheapest and Second-Cheapest Silver

Multiple caveats are in order. First, rates requested do not equal rates approved. Second, the average spread in a given state masks differences in different rating areas within that state. Third, a modest increase in the percentage of income that subsidized buyers will be asked to pay for the benchmark may roughly equal the average increase in "silver discount" indicated here. Fourth this is a sampling of just nine states (including DC). And finally, almost half of individual market enrollees are unsubsidized, and to them, the spread will vary by age. For those with incomes over 250% FPL, subsidized or unsubsidized, the spread will not pack the extra wallop of providing access to CSR at a discount.

Nonetheless, the snapshot is at least suggestive. Intense competition to offer cheapest silver does limit price increases at the bottom of the silver spectrum -- and last year, the average spreads between cheapest and benchmark silver did widen slightly. Perhaps coincidentally, CSR takeup seems to have risen in the 38 states that used HealthCare.gov in 2016.

All politics may not be local any more, but the ACA marketplace definitely is.

UPDATE 6/15: Today the Kaiser Family Foundation released an analysis of requested benchmark silver and cheapest silver prices in the largest urban areas in 14 states that have provided enough information to do such analysis. In eight out of fourteen, the requested rates for cheapest silver went up more than for the benchmark. On average, the cheapest silver request was up 11% and the benchmark, 10% -- the reverse of the Avalere comparison, in which the average requested benchmark increase was a percentage point higher than the average cheapest silver increase. In sum, local variation is tremendous, and the relationship between cheapest silver and benchmark silver pricing is probably pretty random, except in cases in which one insurer grabs both slots, which is not uncommon (and generally spells a negligible spread).

----

* According to the Kaiser Family Foundation's latest nongroup market survey, 64% of all nongroup market enrollees are in marketplace plans. 83% of marketplace enrollees are subsidized.

The cheaper silver plans may turn out to be skimpier and stingier in ways that are not revealed by price alone. Also less stable, although all ACA plans are becoming less stable year to year.

ReplyDeleteWe have discussed that the cutoffs in subsidies have in effect created a two tier ACA marketplace.....the persons with incomes around 200% of poverty, and in states which expanded Medicaid, who are pretty decently protecte....in contrast to higher

income individuals in all states, who are being walloped with annual price increases just as bad as before the ACA.

A righteous sense of anger is building up in the latter group, and look out below if Trump is elected.