Subscribe to xpostfactoid via box at top right. You'll get 2-3 posts per week, mostly re ACA.

On March 11, the Massachusetts Health Connector became the first ACA marketplace to respond to the flood of job losses triggered by the Covid-19 pandemic by opening an emergency Special Enrollment Period (SEP) in which any uninsured resident could enroll in private market coverage. Eventually, 12 of the 13 state-based exchanges opened emergency SEPs, whereas HealthCare.gov, the federal exchange serving 38 states, declined to do so, though HealthCare.gov has taken steps to ease the normal SEP-for-cause application process.

On May 1, Massachusetts reported that in the SEP's first 40 days, 8,300 state residents had gained coverage specifically through the emergency SEP, while 20,200 in total had enrolled in coverage in March and April -- the bulk of them via ordinary SEPs, in which an applicant reports a life change, usually loss of other insurance, that qualifies her to enroll outside of the annual fall Open Enrollment period.

It's hard to assess the success or impact of the emergency SEPs based on these kinds of data snippets, which several state marketplaces have put out. On the whole, March/April enrollment in Massachusetts represents 6.3% of enrollment as of the end of Open Enrollment in January. That does seem a somewhat elevated off-season pace.* In any case, it's likely that Medicaid will pick up the lion's share of the newly uninsured, and the enrollment report did not include Medicaid numbers.

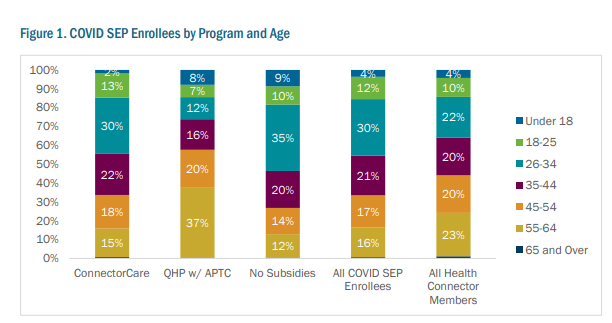

David Anderson seized on one interesting aspect of the report: a high percentage of emergency SEP enrollees are in younger age brackets:

Anderson suggests that the age data should put a touch of downward pressure on 2021 premium rates:

Will the younger enrollees who are coming into the risk pool due to an attention/information/revaluation shock of a global pandemic stick around. They had a revealed preference of either in-attention OR valuation that insurance was not a good enough value relative to premiums to not enroll last November and December, but does a pandemic increase the salience and value of any insurance versus no insurance? I would suspect that is mostly a yes.If the past is prologue, the new enrollees of all ages are likely to "stick around." Retention in the Massachusetts marketplace is very high. That's largely because Massachusetts, which "wraps" state subsidies around federal ACA subsidies at incomes up to 300% FPL, makes coverage far more affordable up to that income level than it is in any other marketplace (though New York's Basic Health Program makes coverage even more affordable in the 150-200% FPL bracket, and Washington, D.C. extends Medicaid eligibility to 210% FPL).

If these folks do stick around, they should lower the average risk and thus the average gross (pre-subsidized) premium by a smidge. This is one of the many questions that actuaries are trying to figure out right now as rates are being prepared for 2021.

Three quarters of the SEP enrollees -- and three quarters of MA marketplace enrollees generally -- are enrolled in ConnectorCare, the program for enrollees with incomes up to 300% FPL (that's $37,470 for an individual, $77,250 for a family of four). In ConnectorCare there's only one metal level, silver (state subsidies also "wrap around" federal Cost Sharing Reduction subsidies, available only with silver plans), and only one fee schedule. Here's what ConnectorCare enrollees get, compared to marketplace enrollees in other states:

ConnectorCare vs. Marketplace Benchmark Silver: Enrollee Costs

Income

(FPL)

|

C-Care premium

|

Marketplace

maximum

benchmark

premium

|

C-Care

deductible

|

Marketplace

average. benchmark

deductible

|

C-Care

Med/drug

OOP max

|

Marketplace

highest allowable

OOP max

|

|

0-100%

|

$ 0

|

$ 21

|

$0

|

$ 209

|

$0

|

$250

|

$2700

|

100.1-150%

|

$ 0

|

$ 64

|

$0

|

$ 209

|

$750

|

$500

|

$2700

|

150.1-200%

|

$ 43

|

$ 135

|

$0

|

$ 762

|

$750

|

$500

|

$2700

|

200.1-250%

|

$ 82

|

$ 216

|

$0

|

$3268

|

$1500

|

$750

|

$6500

|

250.1-300%

|

$123

|

$ 305

|

$0

|

$4546

|

$1500

|

$750

|

$8150

|

Sources: Kaiser Family Foundation on cost-sharing

and benchmark

premiums; MA

Health Connector

Marketplace benchmark premiums are quoted at the top of each income bracket

Marketplace benchmark premiums are quoted at the top of each income bracket

Lower premiums, no deductibles, out-of-pocket maximums very low by U.S. standards...ConnectorCare, descended from the Massachusetts health reform program that predated and presaged the ACA, is the ACA as it should have been. Pre-Covid-19-crisis, the state uninsured rate was 2.8%, the lowest in the nation (the state also enacted the ACA Medicaid expansion, which extends Medicaid eligibility to adults with incomes up to 138% FPL).

Because ConnectorCare plans are in the same risk pool as plans offered at incomes above 300% FPL, and because they're cheap enough to attract a younger, healthier population than the ACA norm, Massachusetts also has the lowest average unsubsidized premiums in the nation. Retention has accordingly been high across the income spectrum:

Massachusetts' relatively affordable and competitive marketplace would be hard at this point for other states to replicate, especially as their budgets are crushed by the pandemic-triggered economic crash. ConnectorCare combines the virtues of a Basic Health Program -- low premiums and out-of-pocket costs, made affordable in part by inducing participating insurers to pay low rates to providers -- with the virtue of a single risk pool not only for all individual market enrollees, but for all individual and small group enrollees. As I noted recently, several unique features work in tandem:

The Massachusetts Health Connector controls costs by several means: subsidizing enrollees to a level that improves the risk pool; committing state resources to advertising and outreach; requiring higher MLR of insurers; standardizing plan design and reducing choice to manageable levels; and requiring insurers to compete to offer ConnectorCare plans, as the state chooses only five participants in that submarket annually (see p. 13 here). Because the lowest-cost silver plan is the one at which quote ConnectorCare premiums are available, insurers compete for this position, which keeps silver premiums low. The benchmark plan picks up all auto-enrollees, i.e. those who don't actively choose a plan.One peculiarity of the emergency SEP enrollment figures is that younger-adult enrollment is really high among unsubsidized as well as among ConnectorCare enrollees. I have not been able to determine whether 18-34 enrollment in ConnectorCare is normally as high as in the SEP figures. The high concentration of younger adult enrollment in the unsubsidized market is unusual, though the numbers are small -- about 1700 new enrollees. Anderson's retention question may be most salient with this group -- though those at the upper end of ConnectorCare eligibility may find even the relatively low premiums challenging in hard times. In fact, as in all marketplaces, a good number of ConnectorCare enrollees may transfer into Medicaid as their incomes drop.

--

* Charles Gaba has dredged up a one-time yardstick for SEP enrollment in normal times: For 2015, HealthCare.gov reported an average of about 6,000 off-season enrollments per day. Two months at that pace would constitute about 4% of end-of-OE enrollment in that year, whereas Massachusetts' March-April total represents 6.3% of end-of-OE enrollment. That comparison may not mean anything; for one thing, we don't know how SEP enrollment varied by season in 2015, or how it varies now for that matter. We do know that total enrollment in HealthCare.gov states tends to drops at a fairly even pace all year (see monthly enrollment chart in this post), but it could be that disenrollment and enrollment ebb and flow together.

A family of four with an income up to $77,250 a year can get zero deductibles? Wow.

ReplyDeleteAt least half the enrollees on corporate health plans would be better off if their employers stopped offering insurance altogether.

I do appreciate that salaries and living costs are higher in Massachusetts. Here in rural MN, a family income of $77K is well above average.