As the ACA-compliant individual market shuddered under a second consecutive round of premium hikes averaging well north of 20% in 2018, I took in an earful of stories from people in their fifties and sixties who were paying full freight, partly recounted here.

One thing that struck me somewhere along the way is the impact of the personal inflation hit induced simply by aging. In the best of markets, late-middle-agers will pay 4-5% more in many years simply for getting a year older. That's a turbo-charge to double-digit hikes for everyone (particularly for couples).

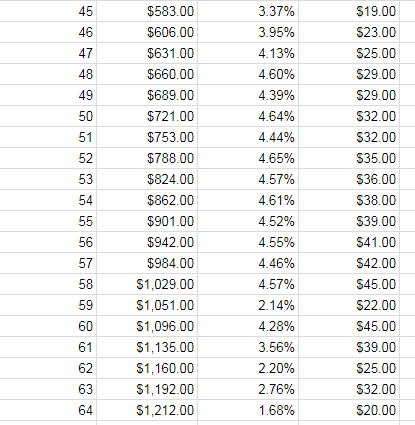

David Anderson, who may do a more analytical post about this, was kind enough to pull an ACA age rating chart for me. I begin at age 45, just before price increases accelerate. This is for one bronze plan in Arizona:

Age Premium Age-related increase Premium change

The sweet spot for premium hikes (reminiscent of the prime years of a ballplayer with a long career) is ages 48-58. Of course the increases compound like interest: 4.6% of $984 is considerably more than 4.6% of $631.

Subsidized enrollees in the ACA marketplace are held harmless from this personal inflation. A 58 year-old with an income of $24,000 pays the same price for a benchmark silver plan as a 28 year-old at the same income. In fact, since the subsidy needed to bring the older enrollee's share of the premium to that fixed level (about $125/month at $24k income) is so much larger, that subsidy may cover much more the premium for a plan cheaper than the benchmark (bronze, cheapest silver, or, in some cases in the current CSR-addled market, gold). But for the unsubsidized, the current level of age rating is bound to intensify the perception of coverage erosion.

Republicans have been chomping at the bit to increase age rating -- the extent to which premiums for the oldest buyers can exceed those for the youngest -- from the ACA's 3-to-1 up to 5-to-1, the pre-ACA norm. That would of course exacerbate the plight of unsubsidized 50- and 60-somethings. Below is a conversion chart showing the effects of going from 3-to-1 to 5-to-1, courtesy of Milliman:

Making that switch after two years of steep premium hikes, with more on the way (thanks to mandate repeal and the loosening of restrictions on ACA-noncompliant plans) would virtually compel further change -- either going whole-hog with an underwritten, lightly regulated market or capping premiums in the ACA-compliant market as a percentage of income for all comers.

Making that switch after two years of steep premium hikes, with more on the way (thanks to mandate repeal and the loosening of restrictions on ACA-noncompliant plans) would virtually compel further change -- either going whole-hog with an underwritten, lightly regulated market or capping premiums in the ACA-compliant market as a percentage of income for all comers.

One thing that struck me somewhere along the way is the impact of the personal inflation hit induced simply by aging. In the best of markets, late-middle-agers will pay 4-5% more in many years simply for getting a year older. That's a turbo-charge to double-digit hikes for everyone (particularly for couples).

David Anderson, who may do a more analytical post about this, was kind enough to pull an ACA age rating chart for me. I begin at age 45, just before price increases accelerate. This is for one bronze plan in Arizona:

Age Premium Age-related increase Premium change

The sweet spot for premium hikes (reminiscent of the prime years of a ballplayer with a long career) is ages 48-58. Of course the increases compound like interest: 4.6% of $984 is considerably more than 4.6% of $631.

Subsidized enrollees in the ACA marketplace are held harmless from this personal inflation. A 58 year-old with an income of $24,000 pays the same price for a benchmark silver plan as a 28 year-old at the same income. In fact, since the subsidy needed to bring the older enrollee's share of the premium to that fixed level (about $125/month at $24k income) is so much larger, that subsidy may cover much more the premium for a plan cheaper than the benchmark (bronze, cheapest silver, or, in some cases in the current CSR-addled market, gold). But for the unsubsidized, the current level of age rating is bound to intensify the perception of coverage erosion.

Republicans have been chomping at the bit to increase age rating -- the extent to which premiums for the oldest buyers can exceed those for the youngest -- from the ACA's 3-to-1 up to 5-to-1, the pre-ACA norm. That would of course exacerbate the plight of unsubsidized 50- and 60-somethings. Below is a conversion chart showing the effects of going from 3-to-1 to 5-to-1, courtesy of Milliman:

The libertarians would say that we should all have a well funded HSA account by the time we are 55, in order to help pay those larger premiums.

ReplyDeleteExcept that most people don't.

Of course Medicare has no age ratings like this. A 95 year old pays the same Part B premium as a 65 year old. Social insurance does not penalize the old.