UPDATE, 10/28/17: The main glitch identified in this post -- the HealthCare.gov "preview plans" tool's failure to calculate the subsidy accurately for households in which not all members are seeking marketplace insurance - was fixed in the late hours of 10/27. The second glitch identified below, pertaining to CSR, is unlikely to be fixed.

---------

People concerned with the functioning of the ACA marketplace were pleasantly surprised yesterday when HealthCare.gov's "Preview 2018 Plans & Prices" tool went live a week in advance of the launch of Open Enrollment. And as I noted a couple of weeks ago, the information flow on the site is streamlined and well-designed, routing visitors as appropriate to check their eligibility for a special enrollment period for 2017, preview 2017 plans and prices, prep for 2018 enrollment, or apply for Medicaid if their income and state of residence indicates it. It has seemed so far that Trump administration sabotage of the marketplace has not so far extended to the federal exchange.

There are, however, important glitches in the functioning of the preview tool that are likely to seriously mislead some visitors.

The most important glitch was pointed out to me on Twitter (when I pointed out a somewhat more understandable one described below):

An enrollee at this income is supposed to pay about 6.5% of income for the the benchmark (second cheapest) silver plan in his or her area. Instead, the 40 year-old whose spouse has other coverage gets this estimate:

If that seems too good to be true, it's only because it is.

If both members of this couple are subsidy-eligible, here's what they pay for benchmark silver:

That's $2,142 for the year, or 6.49% of income. And in fact, that would also be accurate for the one adult if the other has other insurance, as the same percentage of family is deemed "affordable" for one adult as for two (as Louise Norris -- who else -- clarified for me).

The inability to account properly for family members who are not enrolling in marketplace coverage affects users whose children qualify for CHIP. In Essex County NJ again, a couple aged 40 and 38 with a child, family income $41,000, are quoted a premium of $1.05 per month for benchmark silver.

That's a straight malfunction. A second glitch is a function of the pricing anomalies stemming first from Trump's threat to cut off reimbursement of the Cost Sharing Reduction (CSR) subsidies they're obligated to provide to qualifying enrollees, and then from his actual cutoff earlier this month. Long story short, with insurers now loading the cost of CSR onto silver plan premiums only in many states (because CSR is only available with silver plans), gold plans now cost less than silver in some states. That makes gold a better value than silver for a) enrollees who qualify for premium subsidies but no CSR, and b) enrollees who qualify for premium subsidies and the weakest level of CSR (those in the 200-250% FPL income bracket).

"Weak" CSR raises the actuarial value of a silver plan from 70% to 73%. Gold plans have an AV of 80%. In deductible terms, weak CSR plan deductibles average around $2900, while gold plan deductibles average a bit more than $1000.

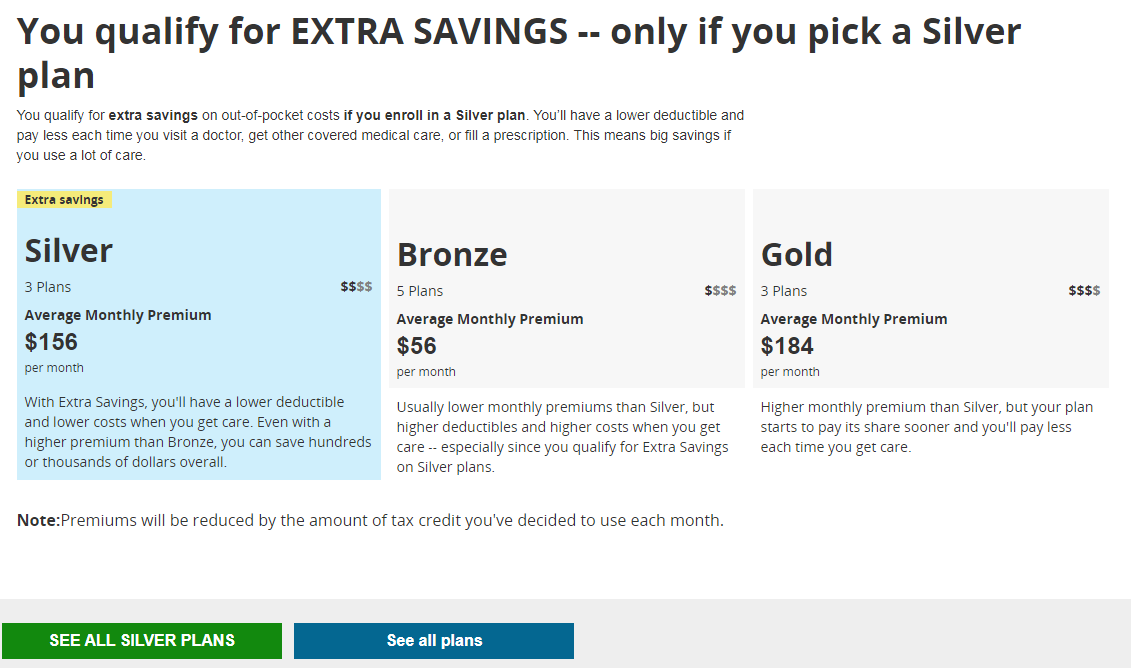

HealthCare.gov's plan preview tool has a useful feature: it alerts CSR-eligible shoppers that they can access CSR only if they buy silver plans, and it invites them to view silver plans first (to "filter" for silver). The problem is, one now gets that alert and option if eligible for "weak" CSR, regardless of whether a more valuable gold plan is available for less.

In Wichita Kansas, for example, a 40 year-old with an income of $25,000, or 207% FPL, can get a CSR-enhanced silver plan with a deductible of $3200 for $133 per month -- or a gold plan with a deductible of $1500 for $98 per month. For that shopper, however, silver plans are still labeled "extra savings", and she is invited to view silver plans only at a first look at what's available. Here's what it looks like (with somewhat misleading averages of premiums at each metal level highlighted):

If this shopper selects "see all plans," plans are ranked by premium, and a gold plan turns up before any silver, nestled among bronze selections:

Retooling the system to avoid this glitch may be challenging. Fixing the more basic glitch -- showing wrong subsidies for households in which not all members are eligible for or seeking marketplace coverage -- is absolutely essential

---------

People concerned with the functioning of the ACA marketplace were pleasantly surprised yesterday when HealthCare.gov's "Preview 2018 Plans & Prices" tool went live a week in advance of the launch of Open Enrollment. And as I noted a couple of weeks ago, the information flow on the site is streamlined and well-designed, routing visitors as appropriate to check their eligibility for a special enrollment period for 2017, preview 2017 plans and prices, prep for 2018 enrollment, or apply for Medicaid if their income and state of residence indicates it. It has seemed so far that Trump administration sabotage of the marketplace has not so far extended to the federal exchange.

There are, however, important glitches in the functioning of the preview tool that are likely to seriously mislead some visitors.

The most important glitch was pointed out to me on Twitter (when I pointed out a somewhat more understandable one described below):

Like the Alka Seltzer guy, I tried it, and Mr. Setzler is right. If you enter info for a married couple, and one has access to other insurance, the estimated subsidy is the same. In Essex County, NJ, for a married couple ages 40 and 38 with an income of $33,000 --- slightly over 200% of the Federal Poverty Level -- the estimated subsidy is $633, whether or not one has outside coverage.Try a married couple with spouse on Medicare. Subsidy estimate is way too big and every plan is free, even if more expensive than benchmark.— Brian Setzler (@BrianSetzler) October 26, 2017

An enrollee at this income is supposed to pay about 6.5% of income for the the benchmark (second cheapest) silver plan in his or her area. Instead, the 40 year-old whose spouse has other coverage gets this estimate:

If that seems too good to be true, it's only because it is.

If both members of this couple are subsidy-eligible, here's what they pay for benchmark silver:

That's $2,142 for the year, or 6.49% of income. And in fact, that would also be accurate for the one adult if the other has other insurance, as the same percentage of family is deemed "affordable" for one adult as for two (as Louise Norris -- who else -- clarified for me).

The inability to account properly for family members who are not enrolling in marketplace coverage affects users whose children qualify for CHIP. In Essex County NJ again, a couple aged 40 and 38 with a child, family income $41,000, are quoted a premium of $1.05 per month for benchmark silver.

That's a straight malfunction. A second glitch is a function of the pricing anomalies stemming first from Trump's threat to cut off reimbursement of the Cost Sharing Reduction (CSR) subsidies they're obligated to provide to qualifying enrollees, and then from his actual cutoff earlier this month. Long story short, with insurers now loading the cost of CSR onto silver plan premiums only in many states (because CSR is only available with silver plans), gold plans now cost less than silver in some states. That makes gold a better value than silver for a) enrollees who qualify for premium subsidies but no CSR, and b) enrollees who qualify for premium subsidies and the weakest level of CSR (those in the 200-250% FPL income bracket).

"Weak" CSR raises the actuarial value of a silver plan from 70% to 73%. Gold plans have an AV of 80%. In deductible terms, weak CSR plan deductibles average around $2900, while gold plan deductibles average a bit more than $1000.

HealthCare.gov's plan preview tool has a useful feature: it alerts CSR-eligible shoppers that they can access CSR only if they buy silver plans, and it invites them to view silver plans first (to "filter" for silver). The problem is, one now gets that alert and option if eligible for "weak" CSR, regardless of whether a more valuable gold plan is available for less.

If this shopper selects "see all plans," plans are ranked by premium, and a gold plan turns up before any silver, nestled among bronze selections:

Retooling the system to avoid this glitch may be challenging. Fixing the more basic glitch -- showing wrong subsidies for households in which not all members are eligible for or seeking marketplace coverage -- is absolutely essential

Thanks for flagging this error. We have manually corrected for it by running coverage scenarios for parents alone, while matching their %FPL to the whole family's %FPL.

ReplyDeleteI have never used the federal website to calculate subsidies in my agency. I use a separate site like the one created by Kaiser.

ReplyDeleteThe hc..gov "see plans" tool is actually well designed and should work well, assuming they fix this glitch...but it wouldn't work for you in Minnesota, would it? The MN site has always been one of the least usable with respect to previewing plans and prices with subsidy.

ReplyDelete