Note: Free xpostfactoid subscription is available on Substack alone, though I will continue to cross-post on this site. If you're not subscribed, please visit xpostfactoid on Substack and sign up.

When considering how the most seismic changes in the ACA marketplace’s 13-year history have shaken out, it’s important to keep in mind that the market mainly serves very low-income people. Consider*:

64% of all marketplace enrollees in 2026 had income in the 100-200% FPL range. In the U.S. population at large, just 15% were in that income range as of 2024.

54% of all marketplace enrollment (12,487,037) in 2026 is in ten states that have refused to enact the ACA Medicaid expansion, where eligibility for marketplace subsidies begins at 100% FPL. In expansion states, Medicaid is available to all adult citizens and qualified noncitizens with income up to 138% FPL.

More than half of enrollment in nonexpansion states (6,543,435) is in an income bracket (100-138% of the Federal Poverty Level, or FPL) that would qualify those enrollees for Medicaid in expansion states. Those should-be-in-Medicaid enrollees account for 28% of all marketplace enrollment.

In 2026, 83% of silver plan enrollees nationally had income in the 100-200% FPL range, qualifying them for strong Cost Sharing Reduction (CSR) that raises the actuarial value (AV) of a silver plan to 94% (at incomes up to 150% FPL) or 87% (at income from 150-200% FPL). Nationally, the average AV obtained by silver plan enrollees was 88.6%, justifying the presumption now enforced by several states that silver plans should be priced at a roughly platinum level (90% AV), well above gold (80% AV).

With that low-income skew in mind, I’d like to examine both long-term enrollment trends and shifts in metal selection in 2026, the latter driven mainly (presumably) by expiration of the enhanced ARPA subsidies.

Trends include:

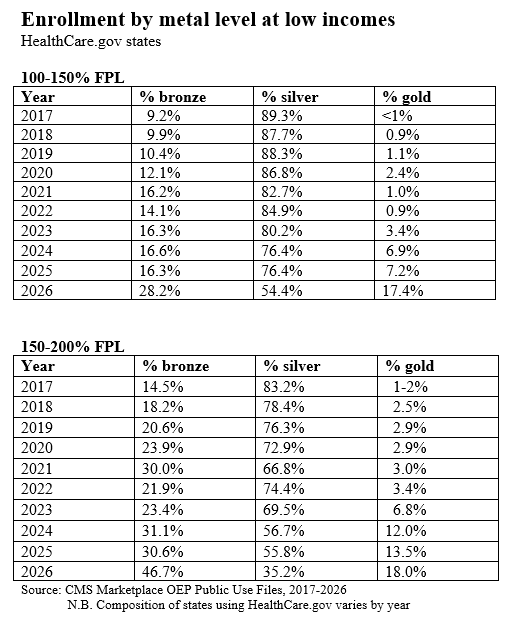

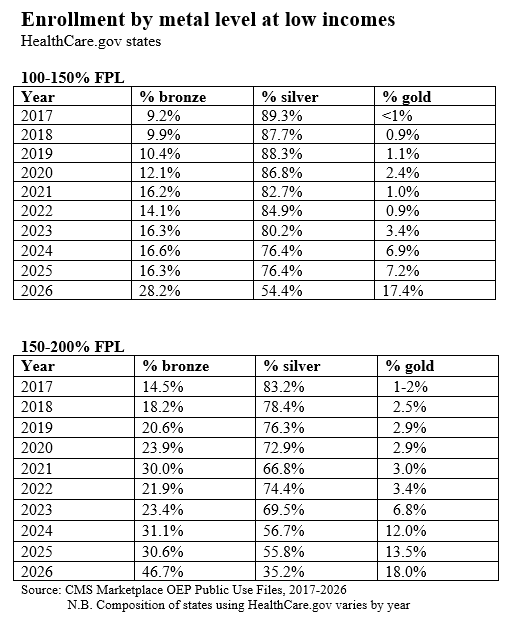

A long-term decline in silver plan selection among enrollees with income below 200% FPL, accelerating in 2026. Selecting bronze or gold plans at incomes up to 200% FPL means forgoing Cost Sharing Reduction (CSR), which raises the actuarial value of a silver plan to 94% (at incomes up to 150% FPL) or 87% (at incomes from 150-200% FPL). At incomes up to 150% FPL, in 2026, silver plan deductibles average $172, vs $7,476 for bronze plans** and $1,722 for gold plans. The annual out-of-pocket maximum (MOOP) for silver plans at this level averages $1,738, whereas bronze and gold plan MOOPs are usually over $8,000.

At low incomes, an increase not only in bronze plan selections in 2026, but also in gold selection, as the availability of zero-premium silver plans all but disappeared, while gold plans in several states — most notably Texas — were available at zero premium.

On net, the average actuarial value obtained by low-income enrollees dropped substantially in 2026, increasing their exposure to high out-of-pocket costs.

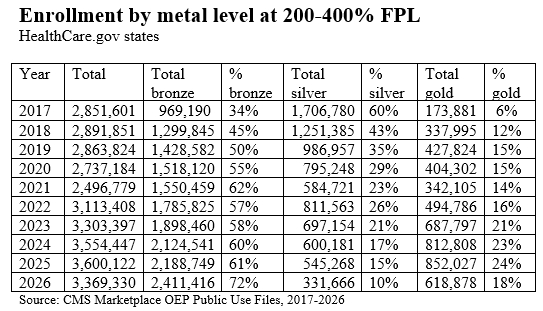

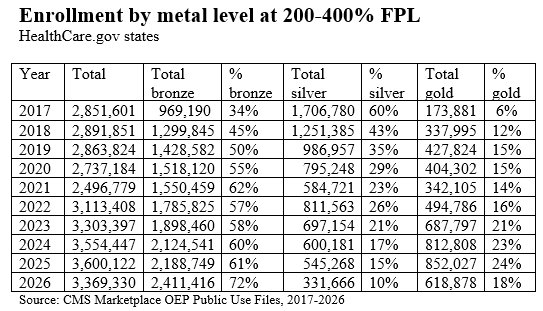

A sharp drop in silver plan selection at incomes over 200% FPL, kicked off by the advent of silver loading (see below…) in 2018. In 2026, higher-income enrollees also shifted from gold to bronze. While silver loading still generates gold plans priced well below silver, the expiration of the ARPA-enhanced subsidies made even those relatively lower premiums too high for many enrollees in the 200-400% FPL income range.

With those basic enrollment facts in mind, let’s consider the effects on enrollment of three high-impact changes to marketplace structure over the years, along with a handful of more gradual trends. First, the major changes:

Trump’s CSR cutoff. In October 2017, Trump abruptly terminated direct reimbursement of insurers for the value of CSR, which attaches to silver plans at incomes up to 250% FPL. In response, insurers priced the value of CSR, which raises the actuarial value of a silver plan to roughly platinum levels at income up to 200% FPL, directly into premiums — mostly into silver premiums, since CSR is available only with silver plans. Since ACA premium subsidies are set to a silver benchmark, with enrollees paying a fixed percentage of income for the second-cheapest (benchmark) silver plan, this change increased subsidies and made plans priced below benchmark cheaper for enrollees. This “silver loading” boosted enrollment while reducing silver plan selection. When silver loading started in 2018, the drop in silver plan selection was immediate and dramatic at incomes over 200% FPL, where CSR is negligible or unavailable. Silver selection eroded more gradually at incomes below 200% FPL, reducing takeup of high-CSR plans with (relatively) low out-of-pocket exposure.

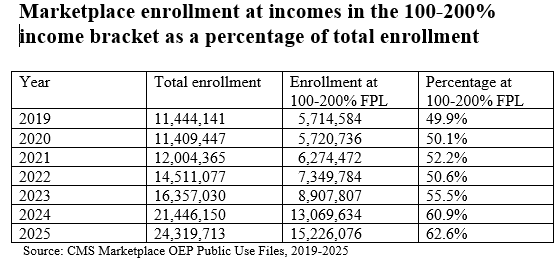

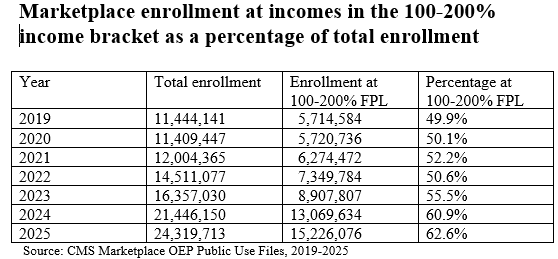

ARPA subsidy boost. The American Rescue Plan Act, enacted in March 2021, immediately and dramatically increase both the size and availability of premium subsidies — ostensibly as a temporary pandemic measure, funded through 2022, and then extended by the Inflation Reduction Act through 2025. Enrollment doubled from 2021 (12.0 million) to 2025 (24.3 million). Most famously, the ARPA enhancements removed the income cap on subsidy eligibility, making benchmark silver available at no more than 8.5% of income regardless of the enrollee’s income level. That boosted the percentage of enrollees receiving premium subsidies from about 80% to about 90%. But the most impactful changes were at lower income levels. Enrollment at 100-200% FPL rose from 6.3 million in 2021 (52% of all enrollment) to 15.2 million in 2025 (63% of total enrollment). Low-income enrollment was boosted by the Biden administration’s enactment in early 2022 of a year-round automatic Special Enrollment Period (SEP) for people with income up to 150% FPL — effectively allowing year-round enrollment, as well as year-round plan-switching.

The Trump administration terminated this year-round low-income SEP in August 2025. That will affect average monthly enrollment in 2026, as enrollment is presumably not being replenished year-round as in 2022-2025.

ARPA enhanced subsidy expiration. It needs no recounting here how the Republican Congress has so far refused to extend the ARPA subsidy increases that expired as of Jan. 1, 2026 (to be fair, the 50-50 Democratic Senate “majority” in 2022 also lacked the oomph to make the ARPA subsidies permanent). So far, the drop in enrollment is less than most observers expected with OEP 2026 enrollment about 5% below OEP 2025. That drop could be wholly accounted for by the lawfully present noncitizens from whom Republicans stripped subsidy eligibility in their July 2025 megabill. But attrition will probably bring average monthly enrollment in 2026 well below 2025 levels, because a) net-of-subsidy premiums are much higher this year, b) year-round enrollment for low-income enrollees has been terminated, and c) individually granted SEPs require documentation more frequently than in recent years.

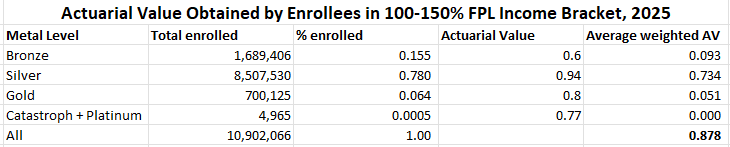

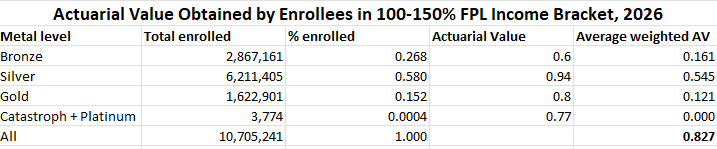

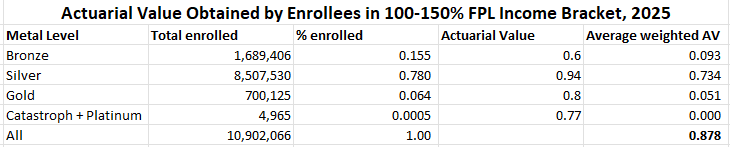

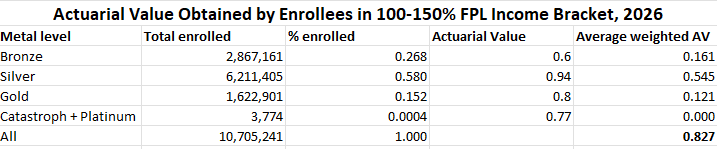

In September 2025, KFF calculated that if the enhanced premiums expired, subsidized enrollees in 2025 would see premiums for the benchmark silver plan in their area (the second-cheapest silver plan) increase by an average of 114% in 2026. That estimate was somewhat juiced by the plight of those who lost subsidy eligibility entirely, for whom premiums could increase by 3-fold, 5-fold, or more. Subsidized enrollment was down 11% in 2026, while unsubsidized enrollment increased by 1.2 million. Among the subsidy-eligible, the average net-of-subsidy premium paid by enrollees rose 30%, from $74/month in 2025 to $96/month in 2026. Among all enrollees, premiums paid by the enrollees increased by 57.5% from an average of $113/month in 2025 to $178/month in 2026. That’s still well below KFF’s estimate of the average benchmark premium increase, net-of-subsidy ($114/month). That’s mainly because of a large-scale shift from silver to bronze at all incomes —- and in some states, from silver to gold at incomes below 200% FPL, where silver plans have higher actuarial value than gold. As I noted previously, the average weighted actuarial value obtained by marketplace enrollees dropped from 80% in 2025 to 76% in 2026 — an all-time low for the marketplace. As AV represents a percentage of total medical costs incurred, and those costs keep rising faster than inflation, the drop in AV obtained exacerbates the steady rise in out-of-pocket exposure. In other words, underinsurance in the marketplace increased substantially in 2026.

Alongside those three jolts to marketplace conditions (the first and third of which drove base premium increases of more than 25% in 2018 and 2026), these long-term trends have also shaped the marketplace:

Narrowing networks. Competition among insurers, touted at the ACA’s inception as a means of holding down costs, probably has done so — but at a cost to network adequacy, as insurers whose primary prior business was Medicaid managed care (e.g., Centene, Molina) showed the way to market share and profitability. Narrow networks are the marketplace norm — and CMS’s risk adjustment formula tends to favor them. Though it’s hard to quantify, I believe that the prevalence of narrow networks in the lowest-priced silver plans has progressively led many enrollees to choose a lower metal level (usually bronze) with eyes wide open to obtain a desired provider network or drug formulary.

Increasing silver loading. Before Trump kicked off the silver loading era by ceasing direct reimbursement to insurers for CSR, that move had been anticipated and analyzed, as the Republican Congress had refused to fund those CSR payments and challenged the Obama’s unfunded payment of them in court. Analysts, beginning with CMS in December 2015, anticipated that gold plans would be priced below silver, because CSR makes silver plans platinum-equivalent for most enrollees. That happened slowly, and unevenly, as competition to offer benchmark silver (along with risk adjustment distortions, according to some) drove many insurers to underprice their silver plans. Increasingly, however, states are mandating that plans be priced in strict proportion to actuarial value — or even that silver be priced as if no one with income over 200% FPL will choose it (a self-fulfilling prophecy in Texas, where just 1% of silver plan enrollees have income over 200% FPL in 2026). In 2018, the first year in which CSR was priced into silver plans, the lowest-cost gold plan premium averaged 109% of the benchmark silver premium, and lowest-cost gold was priced below benchmark (on average) in just 7 states. In 2026, lowest-cost gold plans are priced at 98% of benchmark silver on average, and lowest-cost gold is priced below benchmark silver in 21 states.

Broker pile-in. Brokers have always been essential to marketplace enrollment — given the difficulty and complexity of completing an application; the gutting of funding for enrollment assistance and marketing in the first Trump administration; and widespread, persistent ignorance of the ACA marketplace’s offerings or even existence (abetted by Republican hostility). The first Trump administration wisely encouraged and facilitated broker participation

(while foolishly defunding and denigrating government-sponsored nonprofit enrollment assistance), in part by facilitating development of commercial e-broker platforms that could complete enrollments with subsidies credited. After the ARPA subsidy enhancements vastly increased the availability of zero-premium coverage, brokers piled into the market. In Healthcare.gov states, the percentage of enrollments assisted by brokers rose from just under half in 2020 to 77% in 2024 (and 76% in 2026). In states with their own marketplaces, broker assistance rates vary and are generally lower.

The broker influx has been a mixed blessing. On the one hand, most enrollees need well-informed assistance to navigate the marketplace, most Americans are only dimly aware at best of what’s available in the marketplace until they need it, and broker outreach has reached deep into low-income populations, especially in states that have refused to expand Medicaid, where millions more people (those with income in the 100-138% FPL range) are eligible for subsidized marketplace coverage than in expansion states. On the other hand, the combination of zero-premium coverage availability, the ability to switch plans monthly at incomes up to 150% FPL, and ridiculously easy broker access to enrollees’ accounts via e-broker platforms opened the door wide to broker fraud, which metastasized in HealthCare.gov states in 2023 and 2024 and has been only partially quelled by CMS in 2025 and 2026. A subindustry of high-volume/low ethics call centers has sprung up — centered mainly in Florida, long a hotbed of insurance fraud of all kinds. While trying various methods of crackdown, CMS has so far declined to mandate the kind of relatively simple 2-factor authorization, requiring enrollee input, that’s in effect in most state-based marketplaces, where broker fraud is by all accounts extremely rare.

When broker fraud happens, it usually takes the form of unauthorized plan-switching, which in OEP 2026 could be done up to January 15. When fraudster brokers do this, breaking into an account and switching the enrollment to a different plan, they often move the enrollee to a bronze plan, since the enrollee may not notice the switch if there is no premium to pay (thanks largely to silver loading, bronze plans are still available to many for zero premium). Broker fraud may therefore be a factor in the shift to bronze enrollment.

The Ten Year War over the ACA that Jonathan Cohn wrote about in 2021 is now a 16-year war, with combat unabated. Republican refusal to extend the enhanced subsidies, stripping of subsidy eligibility from most immigrants who lack green cards, and new regulatory barriers to enrollment are reducing the value of coverage obtained by enrollees as well as the number of people enrolled. Yet the marketplace has so far proved more resilient than many anticipated, though the full impact of changes wrought by the Trump administration and Republican Congress affecting 2026 enrollment won’t be visible until we average monthly enrollment for this year is published in mid-2027.

Update: Louise Norris mentioned some days ago that she was looking at metal level selection by enrollment status (active re-enrollment, passive re-enrollment, or new enrollment), and just now, after a conversation with Charles Gaba, I took a peek (it’s in the “State, Metal Level and Enrollment Status” PUF). It’s food for thought.

New enrollees are heavy into bronze. I recall from Covered California’s enrollment data, which has broken out new enrollment for years, that new enrollees tend to go for bronze there too. Perhaps marketplace experience drives one to seek lower out-of-pocket exposure. It’s also not surprising that active re-enrollees tended to shift out of silver this year, when net-of-subsidy premium rose so sharply.

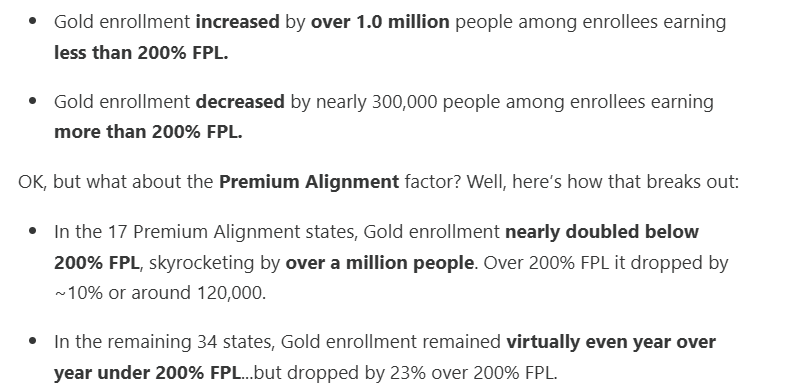

Update, 4/11/26: Charles Gaba adds some interesting perspective on the effect of strict silver loading (his preferred term is “premium alignment”) on metal level choice.

From 2025 to 2026 nationally, Charles notes:

Regarding the drop in gold enrollment at incomes over 200% FPL in states where gold plans are cheaper than silver, I would add: in states that newly introduced strict silver loading in 2026, gold enrollment went up at this income level, whereas it dropped in most states that had silver loading in place prior to 2026. In states where the cost ratio between silver and gold plans stayed roughly the same, gold plans became much more expensive in 2026, thanks to the expiration of the ARPA enhanced subsidies. In states where strict silver loading was newly introduced in 2026 — Arkansas, Illinois and Washington — gold plans were much cheaper in 2026 than previously. In Arkansas, gold plan enrollment at incomes over 200% FPL more than tripled in 2026, from 7,488 to 25,470; in Illinois, it more than doubled, from 29,456 in 2025 to 73,001 in 2026; and in Washington it doubled, from 53,838 to 110,903.

Gold plan selection in those three states rose even more dramatically at incomes under 200% FPL — sucking some enrollees out of CSR silver but again, probably keeping a good number out of bronze or preventing their disenrollment. In Arkansas, gold enrollment at incomes under 200% FPL went from near zero (472) in 2025 to 24,791 in 2026; Illinois told a similar tale, with gold enrollment below the 200% FPL threshold rising from 2,519 to 64,271; and in Washington, the jump was tenfold, from 4,003 in 2025 to 40,570 in 2026.

___

*All statistics cited in the post are derived from CMS’s Marketplace Open Enrollment Public Use Files unless otherwise indicated.

**It should be noted that some bronze plans have $0 medical deductibles — including 11% of all bronze plans (unweighted) in 2026. Since bronze plan actuarial value can’t exceed 65%, the zero deductible generally entails high separate deductibles for drugs, or hospital co-pays of $3,000.

No comments:

Post a Comment